Short-Run and Long-Run Equilibrium

Introduction

Alfred Marshall emphasized the significance of time element in the value theory. According to Marshall, price determination without including time element in the process is meaningless. In order to make the value theory more relevant, Marshall classified time into short-run and long-run. These two time elements have their own peculiarities, which can influence the equilibrium prices.

How does time matter in the determination of equilibrium prices?

To understand the concept better, let us consider the case of perfect competition.

Short-run

In the short-run, as the name indicates, the time is too short to make changes. Therefore, the size of the plants, number of firms, technological factors and resources are fixed. Generally, there are two types of factors of production: fixed factors and variable factors. Fixed factors cannot be modified in the short-run. Therefore, production can be increased or decreased only by changing the size of variable factors. In addition, supply of products is limited by the existing size of the plant. In this case, demand relatively plays a vital role in determining the equilibrium price. The equilibrium based on this situation is known as short-run equilibrium.

Long-run

In contrast to short-run, the size of the plants, number of firms, technological factors and resources are all variables in the long-run, as there is sufficient time for the necessary changes to take place. Here, firms obtaining excess profits seek to expand their production capacity. Also, entry of new firms occur because of excess profits. As number of firm increases, the excess profits start decreasing. Therefore, all firms start earning the normal profits. Entry of new firms beyond this stage results in loss. Equilibrium based on this situation is known as long-run equilibrium.

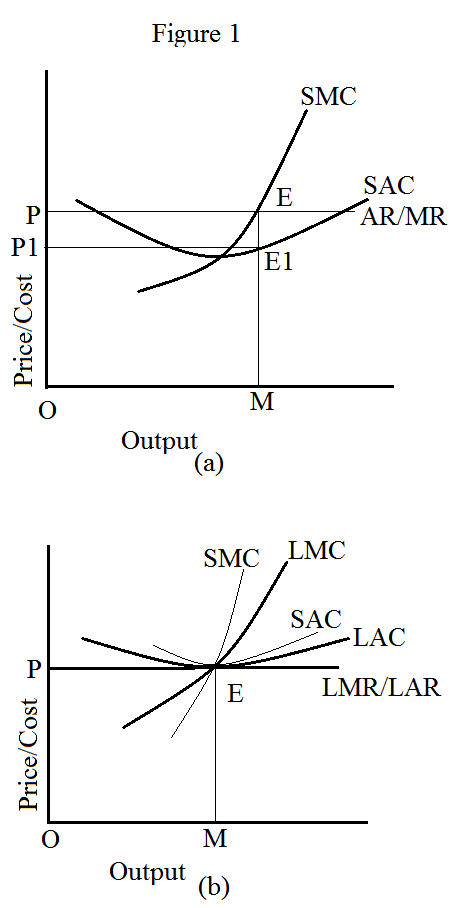

Graphical Illustration

The following picture depicts the equilibrium position of a firm under perfect competition in the short-run and long-run:

Figure 1(a) represents the short-run equilibrium. In the short-run, a firm attains equilibrium when marginal cost is equal to marginal revenue (MC=MR). Since there is low competition in the short-run, the firm can make abnormal profits. The abnormal profits are denoted by the area PP1E1E in the diagram. Due to abnormal profits, the firm is willing to stay at the equilibrium and has no tendency to deviate from it.

Now let us look at the long-run equilibrium. Figure 1(b) represents the equilibrium in the long-run. In the long-run, a firm attains equilibrium when long-run marginal cost is equal to long-run marginal revenue (LMC=LMR). Furthermore, at this point, long-run average cost is equal to long-run average revenue (LAC=LAR). This implies that the firm enjoys only normal profits. In the picture, ‘E’ denotes equilibrium point.

Concept of ‘Early Entry and Early Exit’

The concept of short-run and long-run equilibrium has an important practical implication. Under perfect competition, a business venture is successful when it is started at the right time and at the right place. Here, ‘right time’ implies short-run (i.e. early entry). In the short-run, competition is very low. Hence, when you enter into a business at this stage, you enjoy the benefits of monopoly that gives you abnormal profits. Another advantage of entering into a business early is that you have sufficient time to optimize production and to expand business, which helps the firm to sustain in the long-run. As a pioneer, the business has potential to create a strong brand name for its products. Early entry also provides you with the benefits of economies of scale. When you expand business, certain advantages arise. This is known as economies of scale. For example, when you carry few goods in a commercial truck, it may give you normal profits or incur loss. When you utilize the full capacity of the truck, it gives you abnormal profits.

The story of long-run can be illustrated with a simple example. You find an area in which there is no grocery shop. At the same time, you find that the area has good customer base. Hence, you set up a grocery shop in that area. Obviously, it gives you abnormal profits since there is no competition. However, in the long-run, on looking at your business performance, many entrepreneurs enter into the business. Now you start losing the benefits of monopoly. At this stage, you just start earning normal profits or sometimes your business may incur loss. Hence, this is the time to decide whether to continue or exit the business.

© 2013 Sundaram Ponnusamy

Related

Determination of Equilibrium Price and Quantity Under Perfect Competition

How is Price Determined under Monopoly Market?

How Do Income and Substitution Effects Work on Consumer’s Equilibrium for Giffen, Normal and Inferior Goods?

Microeconomics Review: Imports & Exports

Derivation of Short-Run and Long-Run Supply Curves for an Industry