How to manage Inventory ?

In the previous Hub we talked about the different elements of Working Capital with one of them being Inventory. In this hub we’d look at Inventory Management as part of Working Capital Management.

When it comes to Inventory Management we’ve got two distinct approaches to Inventory Management – the Economic Order Quantity Method & the Inventory Management Systems.

The Economic Order Quantity Method considers ordering fixed amounts of inventory from the suppliers each time. The Economic Order Quantity Method argues that there are numerous quantities of inventory that can be ordered from the supplier each time we decide to place an order; for example if we require 1000 units of Tennis Balls each month, we may order them as 10 orders of 100 Tennis Balls each time or 100 orders of 10 Tennis Balls each time or similarly many other possibilities of order quantities.

Why do we need to decide upon an Order Quantity ?

The problem with so many different possibilities of order quantities is that the Inventory Management System involves a few costs & so its not possible to order & then hold different quantities of inventory without incurring these costs.

The most significant of these costs are:

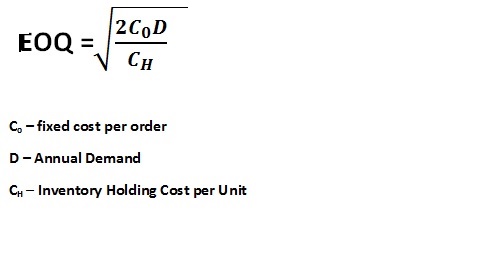

(i) The Purchase Cost : The per unit cost of the Inventory that we incur when purchasing the goods. Normally this cost remains constant throughout the period & therefore is an irrelevant cost when it comes to deciding between different order quantities. However if Discounts are offered for Bulk or Large Quantity Purchases than naturally the Purchase Cost becomes a relevant cost in choosing between different order quantities.

(ii) The Re-Order Cost: These are the costs that we incur every time we place an order. The rationale behind this cost is that every time you place an order you’re incurring costs involved with placing & receiving the order such as Administrative Costs & Delivery Costs.

(iii) The Inventory Holding Cost: These are the costs that are incurred due to holding the inventory for a given period of time. It might include Rent Paid in respect of the Premises used where the Inventory is held or the Insurance Expense that is incurred in respect of the Inventory Held.

The goal of every successful Inventory Management System is to try to order such a quantity every time so as to minimize these costs as much as possible or in other words trying to order the Economic Order Quantity every time. Naturally the lesser the Inventory Management Costs the lesser is the money tied up as Inventory Portion of Working Capital.

So how do we calculate the Economic Order Quantity?

So what do you do when Discounts are Involved?

(i) Calculate the Economic Order Quantity !

(ii) Calculate the Total Inventory Costs i.e Purchase, Re-Order & Holding Cost, at the Economic Order Quantity

(iii) Calculate the Total Inventory Costs at the minimum order quantity required to be eligible for the discount.

(iv) Calculate the Total Inventory Costs at the minimum order quantity required to be eligible for the next discount & so forth if there are more discounts involved

(v) Compare the Total Inventory Costs as per the different Order Quantities & choose the one with the Lowest Total Inventory Costs

So what about the Inventory Management Systems?

When it comes to Inventory Management a lot of systems have been developed & adopted to deal with the management of Inventory. They range from the simple like the Bin System to the more complicated like the Just-in-Time System.

The Bin Systems talks about having a Bin in which the Inventory is held in a single Bin & an Inventory Level is decided upon. The inventory is taken out of that Bin as & when needed & when the Inventory Level on that Bin goes below a certain point fixed quantity of Inventory is ordered & the Bin subsequently replenished.

The Just-in-Time System is a bit more sophisticated system that requires fundamental changes in the procurement, production & sales process to reduce wastages & try to tailor make the product for the customer. As per this Inventory Management System, minimum Inventory Levels are maintained or in other words Minimum or No Inventory is held by the organization & materials are ordered as soon as & as per the customer orders.

The emphasis is on being able to forecast Demand, having a shorter & more efficient production cycle to reduce wastages & to quickly produce as per Order & a reliable source of quality raw materials from the suppliers. What this does is that it reduces Inventory Holding Costs & Wastages drastically & also produces a tailor made product for the customer at a lower price than the organization’s competitors.