What is Term Life Insurance? – the Ultimate Guide to Retirement

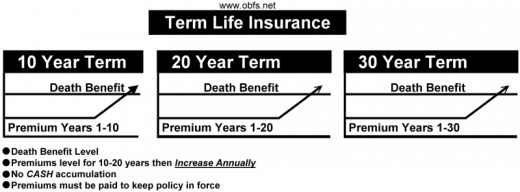

Let’s start with the most fundamental question: what exactly is “term” life insurance supposed to be? A term-based life insurance policy is, as implied by the name, an insurance policy based on providing coverage over a particular period, or a “term.” The policyholder makes annual payments called premiums to the insurance company to keep the policy actively and ensure that the policyholder is secured upon death. It is among the most reasonable of possible life insurance policy types, providing coverage over periods ranging from 1 to 30 years.

Term Life insurance is reasonable and easy to understand. It gives an individual all the coverage he or she need, and they don’t have to worry about what they don't need. That's the reason it is the best choice for almost everybody. Term Life insurance policy is of use for a particular period of time. You get to decide on one year, ten years, twenty years or even up to thirty years. Since everybody generally needs life insurance, it best to pick the term that meets with the time you need coverage. What so great is if you die during that term you select, the chosen beneficiaries get a payout.

It's best to renew a term policy because if you allow your policy to expire without renewal and die, there's no payout. A term life insurance is good to have mainly because it is inexpensive, but their policies typically have maximum issue ages. One major drawback is if you are over 80 years old, you will have a tough time getting a policy. Although, more than likely a person of that age will not need a policy in any case.

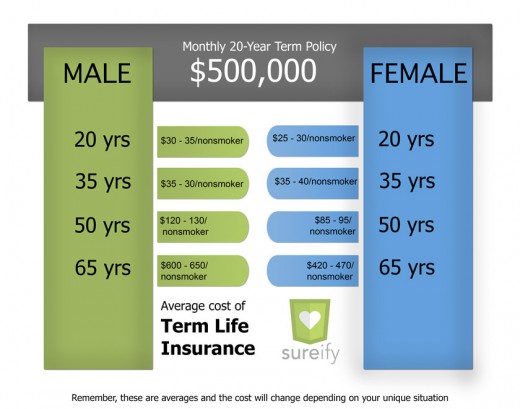

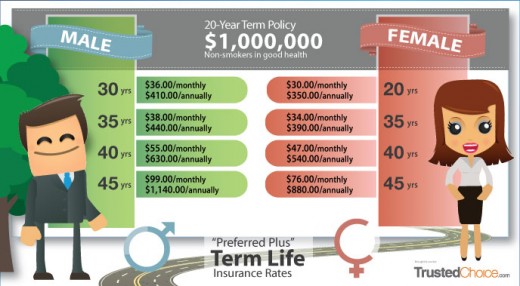

The cost of Term Life insurance policy depends on a personage, the amount of the coverage, an individual health and the length of the benefit they want. With all that being said it should be no surprise that the lower your premium comes with how younger and healthier you are in life.

Can you use Term Life insurance as an effective investment tool?

If you want to start the ultimate guide to retirement you want to invest in IRA or a good 401 (k), it the best way to invest in an investment that serves as a "forced savings." Term life insurance has a retirement plan called cash-value policy. I would not recommend it because it is a very costly way to taken the initiative to invest in a retirement. Starting an ultimate guide to retirement is beneficial in life but if you need life insurance, enter into term insurance. However, if you want to launch the ultimate guide to retirement, invest in IRAs, 401(k)s or idem retirement plans.

How to determine the sizes of the life insurance policy

One of the core rules of an insurance policy is that the life insurance coverage should equal seven to ten times the amount of a person annual salary. However, then again, like any other rule of thumb, that does not make it always accurate.

Also, we can look at it this way: A person needs to figure out the income they want to provide for their family or spouse or the beneficiaries when they die. From that amount, subtract all sources of revenue, and they will be able to select: Social Security, retirement accounts, pensions, for their spouse. The considerable number is the shortage you will want to fill with life insurance.

Now let’s discuss the nine most useful life insurance riders, once you take into account how much life insurance you need, how many years you need it, how much you can afford to spend monthly and what type of policy best fits your situation; your homework still not finish yet, you need an array of life insurance policy add-on known as riders. It a must have and when you purchase a policy and add the riders with it; it can give your policyholders additional benefits and vary from one provider to another giving everybody peace of mind.

There are nine most useful riders you can add to your policy:

1. Guaranteed insurability is a rider that does not require a medical examination, and it is good it does not because as we grow older, our health can fail us. It depends on several factors which are your age, health, and the type of policy you open. Guaranteed insurability will ensure insurability opportunity that will prepare you for life unexpected health failure as we will never know when this could happen.

2. Waiver of Premium is a rider that is treasured by a family because it will ensure the individual if they get injured, falls ill or becomes permanently disabled. This is a handy add-on for the rider to have because with life being of uncertainty a person will never know when hurt or illness could happen.

3. Term Conversion Rider is a rider that is a good add on because of its convenience for young individuals who can only afford a term policy. It allows the conversion of a term policy to turn into a permanent (universal or whole) life policy without the requirement of a health examination. The only disadvantage is it impose a deadline as to when the conversion can be carried out.

4. Accelerated Death Benefit is a rider that allows the insured individual to collect when he or she falls terminally ill and is given limit time to live. This rider is free of charge and can be used for paying hospital bills and everyday expenses. The payout generally falls between twenty-five to forty percent of the death benefit.

5. Disability income is a rider that allows the insured person to collect payment if they have a disability and unable to continue working. How an individual collect depend on the policy because some policy holder will receive disabilities caused by accidents only while another policy holder will obtain both accidents and illnesses.

6. Child protection is a rider that can be used in the unfortunate early loss of a child. It is a convenience policy to have because it helps the family financially. This rider assists the family does not worry about expenses like a funeral and burial charges.

7. Critical illness is a rider that will allow the policyholder to collect a lump amount if he or she gets diagnosed with any illnesses indicated in the policy. Upon diagnoses, the policyholder will receive an upfront sum of money, which can be used for treatment.

8. Accidental death or double indemnity is a rider that will give the policyholder extra benefit that is outside of the ordinary death benefit specified in the policy.

9. Return of premium is a rider that will allow the policyholder to get back most or all of what they paid in premiums, in the case they do not die within the term period. However, if they die the named beneficiaries will get back most or all of what they paid in premiums.

Here is another fundamental question: what are the benefits of having a term life insurance policy? Why would anyone want to have one? Here are a few ways in which choosing a term life insurance policy over another type might suit your needs and lifestyle:

- An enormous amount of flexibility comes from a term policy due to being able to select the time during which coverage is applied. Even the maximum coverage policies are pretty affordable.

- It offers a tax-free death benefit, ensuring that your beneficiary will receive all of the intended funds with minimal interference or hassle.

- If you change your mind, it can be converted into a permanent life insurance policy.

However, this leads to yet another questions. Namely, why would anyone consider term life insurance coverage for 20 years or more? If the coverage is to last that long, wouldn't it be easier - and possibly cheaper, even - to just purchase a permanent insurance policy by that point? As it turns out, there are also many reasons to consider term life insurance over significant periods of time:

A policy for 20 years or more is the best choice to obtain coverage at affordable premiums.

- The policyholder is guaranteed a level premium with the option to renew at a higher premium.

- Policyholders can upgrade to a higher premium without providing proof of good health.

The final fundamental question is for those who are interested in a term life insurance policy: what now? Surely, there must be more to the process than saying “I want a term life insurance policy.” There are, naturally, a few different types of term insurance, each with its own traits.

Five types of term life insurance policies and their benefits:

1. Level Term Life

- Level term life insurance guarantees a policy at a level rate for the policyholder during the term.

- A level amount of life insurance is also guaranteed during the term of the policy.

- Out of all of the types of term life insurance coverage, level term insurance offers the lowest overall rates.

2. Decreasing Term Life

- Decreasing term life insurance also guarantees level rates for the policyholder throughout the duration of the insurance policy.

- Flexible terms and coverage plans are available for time periods ranging from 10 to 30 years.

- Policyholders choosing a decreasing term insurance policy can get proper coverage for a very low rate.

3. Renewable Term Life

- Renewable term life insurance includes the possibility of renewing the coverage so that the policyholder can retain the policy as long as the premium is paid.

- If the policyholder falls ill and becomes unable to pay the premium, the insurer will waive the premium and pay for it in the policyholder’s stead.

- Renewable term life insurance also gives the option of converting the policy to a permanent policy if you so desire.

4. A Convertible Term Life

- Convertible term life insurance guarantees the policyholder conversion and a set benefit for the beneficiary in the event of death.

- Even if the policyholder falls victim to an illness that would otherwise render them ‘uninsurable’, he or she will have the option of converting their policy to another type.

- Before it expires, the policyholder can change the convertible insurance policy to a permanent insurance policy of whatever type is preferred, such as whole, universal, or variable insurance.

5. Return of Premium Term Life

- The return of premium term life insurance policy stands out for one benefit alone: provided that the policyholder is yet living by the end of the term, he or she gets the paid money back.

- The policyholder gets to choose the term during which the premiums are paid monthly, and at the end of that term, the payments are returned.

- This type of policy typically lasts for 20 to 30 years, but the longer the policy is held, the higher the amount of money that gets returned to the policyholder at the end.

For anyone who is in the need of a good insurance policy, the choice of policy type is something that shouldn’t be taken lightly.

Do you have an insurance policy and do you know the important of having great coverage

Retirement Song Music Video.wmv

Term Life Insurance - Cheapest Term Life Insurance

© 2015 Pam Morris