The Truth About ACA Premiums and the Democrats’ Shutdown Demands

One of the major sticking points in the current government shutdown is the Democrats’ insistence on extending the enhanced Affordable Care Act (ACA) subsidies that were first introduced under the American Rescue Plan. Their argument is that, without these subsidies, millions of Americans will see their health insurance premiums skyrocket, to double and triple...

That claim simply does not hold up to scrutiny.

What Actually Happens When Subsidies Expire

What my extensive research shows is that when the enhanced subsidies expire, nothing sudden or dramatic happens on the insurer’s side. Insurance companies do not automatically raise their rates. What actually changes is that the consumer becomes responsible for paying the entire premium again, including the portion that the federal government had temporarily been covering.

To put it simply: before 2021, if someone was paying the full cost of their plan — say, $1,200 per month — that amount remains the true price of the plan. The enhanced subsidy just reduced the customer’s share of the bill.

From 2021 through 2025, during the subsidy period, a customer might have only paid 60% of that cost (around $720/month), while the government covered the remaining $480. When the subsidies end in 2026, that same customer would simply go back to paying $1,200 per month — the original premium — not some artificially inflated number.

While some insurers may increase premiums slightly (as most do each year), current data shows that typical annual increases range from 3% to 6%, driven by healthcare inflation and claims costs — nowhere near 200%.

The Laws That Protect Consumers from Unjustified Increases

There are multiple layers of legal protection built into the ACA and state regulations that prevent insurance companies from arbitrarily hiking premiums. These laws are designed to ensure that any rate increase must be justified, reviewed, and approved before taking effect.

1. Federal Protection: The ACA “Rate Review” Law

Under Section 2794 of the Public Health Service Act (42 U.S.C. § 300gg-94), created by the Affordable Care Act, any proposed premium increase of 10% or more must go through a federal and state review process.

Insurers must submit detailed actuarial data showing why the increase is necessary (for example, due to higher medical costs).

The Department of Health and Human Services (HHS), in coordination with state regulators, reviews the proposal to determine if the increase is “unreasonable.”

If the increase is found unjustified, the insurer must publicly post an explanation and may be forced to withdraw or modify the rate request.

Source: 42 U.S.C. § 300gg-94 — Rate Review

2. State-Level Oversight

Every state has its own Department of Insurance (DOI) that oversees rate filings. These agencies:

Review and approve or reject proposed premium increases before they go into effect.

Require insurers to submit detailed cost data to prove their rates are actuarially justified.

Can deny or reduce rate hikes they find excessive or unsupported by data.

For instance, the Michigan Department of Insurance and Financial Services (DIFS) reviews all ACA rate filings annually. Michigan law requires that premiums reflect actual medical costs, not arbitrary profit-taking.

3. Transparency and Public Accountability

The ACA also mandates public transparency for all rate filings:

Insurers must publish their proposed rate changes on Healthcare.gov and the state’s insurance website.

Consumers can review and comment before final approval.

This level of oversight makes it nearly impossible for insurers to impose sudden, extreme increases without public and regulatory pushback.

Competition Will Keep Prices in Check

As enhanced subsidies end, the market naturally becomes more competitive. When consumers must pay a larger share of their premium, they shop more carefully — and insurers respond by lowering prices or introducing new plans to attract customers.

In fact, smaller or regional insurance companies often enter the marketplace with lower-cost, narrow-network, or telehealth-based plans that can be 10–20% cheaper than major brands. Between 2020 and 2024, the number of insurers offering ACA plans more than doubled, showing that competition is alive and well.

So while some may experience a modest increase when subsidies expire, many others could find new, lower-cost options as companies fight for market share.

The Political Reality

Democrats’ push to permanently extend these subsidies is less about consumer protection and more about entrenching another social spending program. These subsidies were always meant to be temporary, created under the COVID-era relief packages. The Biden administration — and now Democratic lawmakers — are trying to make them permanent, a move that would balloon federal spending by hundreds of billions over the next decade.

President Trump’s renewed commitment to fiscal restraint and cutting unnecessary spending directly opposes this approach. His administration’s position is clear: the government should not continue paying what individuals can pay themselves, especially when the ACA system already includes strong safeguards against unfair pricing.

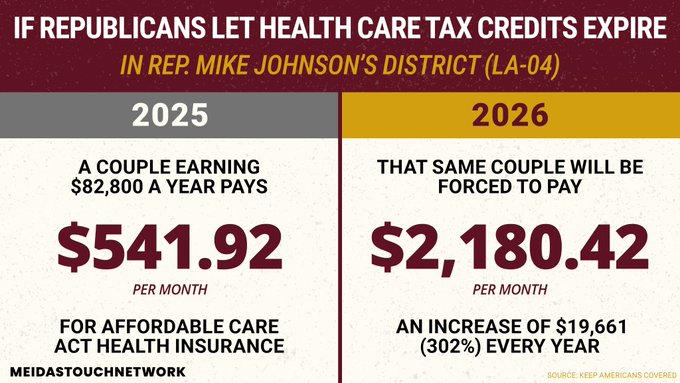

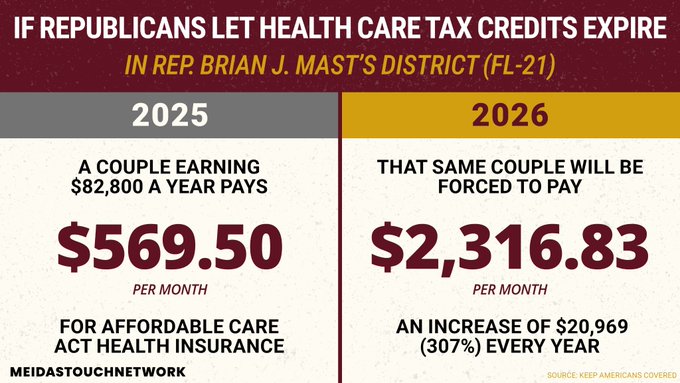

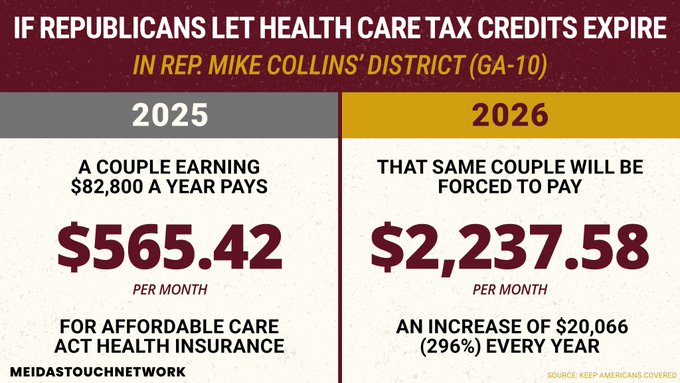

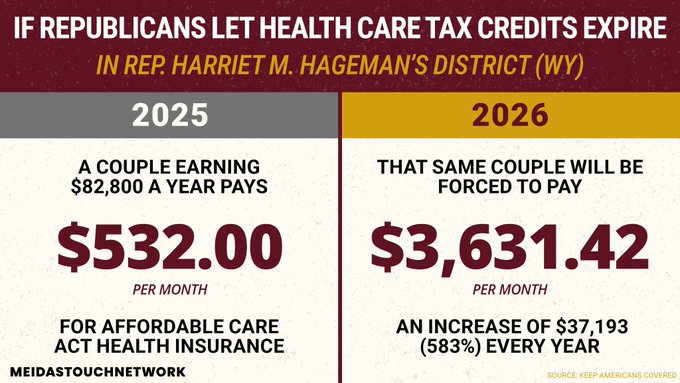

Anyone predicting an outrageous spike in ACA premiums — like 200% or more — is ignoring the facts and the law.