Portfolio Management

Portfolio management is the on-going process of constructing portfolios that balance an investor's ever changing goals with the portfolio manager's assumptions about the future. Within the framework established by the investor’s investment policy, a strategy will be adopted that ensures that the investor’s long-term objective(s) will be attained. Often, the specific tactics that the portfolio manager might employ are also specified. The portfolio is then monitored so that the strategy and tactics can be ad justed to accommodate the outcomes realized and changes in the investor's objectives.

What is the portfolio investment process? The process used to manage portfolios of securities is shown here.

Planning

| ||

|---|---|---|

Policy >>>>>>>>

| Implementation>>>>>>>>

| Monitor

|

The Portfolio Management Process

|

In this article we are just looking at Planning and Policy. Portfolio Management implementation and monitoring will be discussed in the following chapters.

Planning involves assessing the investor's current situation and market conditions to produce a formal statement of investment policy. This includes the investor's optimal strategic asset allocation -- or the portion of assets to be allocated to various types of securities, like stocks, bonds and money market instruments.

The Implementation stage involves acquiring or selling securities, so called portfolio rebalancing, to bring the portfolio into alignment with the policy statement. The last stage is monitoring the performance of the portfolio. Let's look at each stage for important points.

The Investment Policy Statement

These are written objectives agreed upon by the client and portfolio manager and include:

- financial situation

- knowledge or sophistication of the markets

- risk tolerance

- expectations

- uses of investment (college, retirement)

First, let's explore the term investment policy statement or IPS. This refers to the written objectives for the management of a client’s money that are agreed upon by the client and portfolio manager. It is, in many respects, comparable to the job description of an employee. Some considerations in determining the proper asset allocation for retail or non-institutional clients are listed above.

As a side note, the SEC has a suitability rule that requires investment advisors to (1) know their client's financial situation, (2) their client's investment experience (meaning: risk tolerance), and (3) develop, based upon the these factors, an IPS.

Registered representatives, while an agent of the customer, are still required to know their customers. This suitability test ensures that the broker makes inquires about the customer and only makes recommendations appropriate for the individual. Like wise, an investment adviser, a fiduciary, will make inquires about a client’s financial situation and investment experience before advising a course of action recorded by the investment policy statement.

An individual’s investment policy is often based upon the life cycle concept. Portfolio managers assume that during their 20s and 30s, investors marry, have children, and borrow to purchase tangible assets such as a home and its furnishings. Thus, they have a negative or a small positive net worth.

In their 40s and 50s, individuals are assumed to have raised and educated their children and begin investing for retirement. Later, of course, they’re assumed to use their savings for living expenses and thus, their net worth eventually declines.

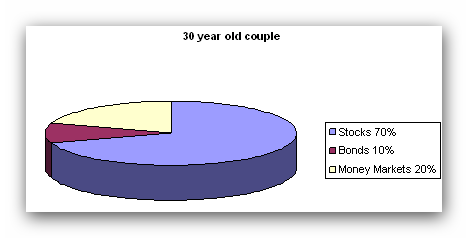

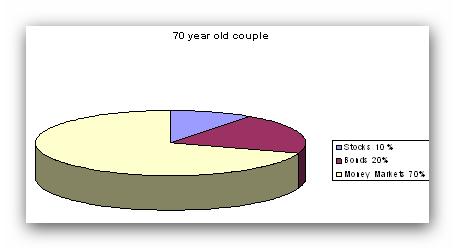

Life Cycle Example

30 year old couple 70 year old couple

long-term horizon short-term horizon

can accept moderate to high risk can accept little investment risk

protect against long-term inflation protect against short-term inflation

Investment Policy of Institutional Investors

The investment policy of institutional investors is more complex. An institutional investor is an investment adviser that either (1) manages large sums of money for corporate, public, and union fiduciaries, including pension funds, or (2) manages large sums of mon ey for individual investors through, for example, a mutual fund.

In this case, policy is based upon the nature of the assets, legal requirements regarding their investment management, tax considerations, and, often, the subjective input of corporate management.

- Nature of Assets

- Legal Requirements

- Tax Considerations

- Corporate Management

The investment advisor must delineate the asset allocation proportions in a policy statement. Strategic asset allocation refers to the percentage of total funds invested in the various security classes, from among these shown. Academic research has shown that more than 90 percent of the variance in the returns of portfolios is attributed to the strategic asset allocation decision.

Strategic Asset Allocation

- money market instruments

- fixed income securities

- equities

- real estate

- international offerings

- Derivative securities - futures, options, warrants, etc.

Before we move on, let’s quickly discuss institutional investors with concerns such as a pension plans Because of tax incentives and competing benefits offered by other employers, many large companies offer investment alternatives for their employees to help plan for retirement. Pension plans today are the single largest owner of common stock in America. The investment management of these funds to ensure adequate funding of retirement benefits is a major business.

Recommended Books on Portfolio Management

The Investment Policy Statement

Is a written set of objectives agreed upon by the client and portfolio manager

- age of employees

- defined benefit

- defined contribution

- current salaries

- number of years to retirement

Age of Employees

The average age of the employees in a corporation defines the length of time the pension fund’s investments will likely have before they are needed. This affects the amount of risk and liquidity a manager can approve for the portfolio in much the same way that an investment manager recommends a different portfolio for a younger individual than for an older individual

Defined Benefit

A defined benefit plan has set benefits. Participants in the fund know exactly now much money they will receive and when. For example, a plan may state that the employee will receive 20% of his or her final salary after 25 years of service. Investment strategies must take this requirement into account. The fund will require a set amount of liquid assets at any given time. If the plan is able to meet the required amount of liquid assets it is considered fully funded.

Defined Contribution

These plans typically involve funds from both the employee and the employer that are invested in a broad portfolio. Upon reaching retirement, employees may draw upon the funds according to a variety of strategies. Unlike the defined benefit plans, the amount the employee may draw depends entirely on the amount invested and the return on the investment. 401K plans are a typical example of defined contribution plans. Investment strategies for these plans may involve input from the plan members. Because there is no set liquidity needed, these plans can often tolerate higher levels of risk.

Current Salaries

Because funds for a pension plan are often deducted as a percentage of the employee’s salary, the current salaries often define the amount of new money an investment manager has at his or her disposal for the current time period. Investment decisions may be based upon this.

Number of Years to Retirement

In defined benefits plans, the number of years after which the employee may retire is of prime importance in calculating the benefits the plan can afford to pay. If this calculation is off, the fund may eventually encounter more liabilities than it can tolerate.

Which of these two plans should be more able to accept short-term market risk and thus should devote a higher percentage of assets into equities?

American Business Machines New York Biotech

Employees 1,000 1,000

Avg. Age 50 35

Avg. Salary 40,000 30,000

Length of Retirement 15 years 15 years

DB/DC defined benefit defined contribution

Current equities assets 45.0 million 1.25 million

% Mix (stock/bond/MM) 60/30/10 25/25/50

Yes you probably worked out that the New York Biotech fund is in a better position to accept risk. It has younger employees and is a defined contribution plan, which means that it does not have to guarantee to make a certain dollar distribution upon retirement.

Which of the plans below is more likely to be under funded, meaning not have enough money set aside to pay for retirement benefits when due?

American Business Machines New York Biotech

Employees 1,000 1,000

Avg. Age 50 35

Avg. Salary 40,000 30,000

Length of Retirement 15 years 15 years

DB/DC defined benefit defined contribution

Current equities assets 45.0 million 1.25 million

Mix (stock/bond/MM) 60/30/10 25/25/50

Only defined benefit plans are funded and therefore liable to retiring employees for a pension benefit. Thus, ABM is the plan more likely to be under funded. New York Biotech, a defined contribution plan, cannot, by definition, be under funded.

Related

System in a Multi-ETF Portfolio")

Using Robert Lichello's Automatic Investment Management (AIM) System in a Multi-ETF Portfolio

System")

A Sensitivity Analysis of the Robert Lichello Automatic Investment Management (AIM) System

21 of the Greatest Investors of All Time

Understanding the P/E Ratio: A Guide for Smart Investors

Contentment: The Greatest Wealth