To Buy or Not to Buy: An Analysis of Home-Ownership in New Jersey

Why Buy a Home?

Even as The Apartment List Renter Confidence Survey (RCS) declares that the renter population is at its peak, as compared to the past 20 years, there are several pragmatic reasons why being a homeowner is an achievement to be proud of. It is the most important long term investment that a person makes and it adds an essential asset to their name. Moreover, it is a sound investment, since the more a home buyer progresses on their mortgage payments, the more equity they accumulate.

Given that the real estate market is mostly stable in the long run, property prices are likely to appreciate, accruing further equity to the owner, which he can either choose to borrow against or cash as profits when he sells his property.

Benefits of Being a Home-Owner

A home owner will also receive tax benefits, with the mortgage interest and property taxes being deductible from the total payable tax, as is enumerated by the analysis presented by Isabella Community Credit Union. Owning a home also gives a sense of security to a person, both financially and emotionally.

Financially, one is able to plan better as personal property has fixed costs, as opposed to a rented establishment; and emotionally, one develops a sense of being rooted and has the freedom to personalize their space in the truest sense. It also affords a person more control over his/her environment, making it conducive to stability.

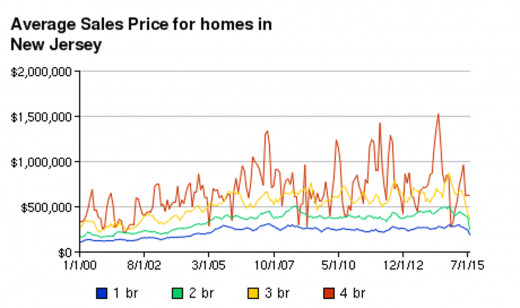

Why Buy a Home in New Jersey?

The Garden State is a popular choice for buying a home, especially due to its proximity to New York. However, that is not the only reason. Real estate in New Jersey has been experiencing a boom since March 2015, according to an article in Housing Wire. The reasons cited by the article include a surge in demand due to low interest rates and lesser down payments sought by Freddie and Fannie. It also speaks of the change in demography of home buyers, namely the single millennial between the ages of 18 and 34, who are looking to secure themselves. This makes it hot property indeed.

Home Loans

It is recommended that you first find yourself mortgage before you choose the house you buy. This is the smart way to go, since it will help you determine what you can afford. What you can afford will in turn be determined by your FICO or Credit Score. Scores can range from 300 to 800 and the higher your score, the more likely you are to be considered for a loan. It is popularly believed that it is very difficult to obtain a loan for a new construction in New Jersey. However, this has been contested by First Equity Mortgage, who suggest speaking to a loan specialist before taking a decision.

What Does the Law Say?

The New Jersey Homeowners Security Act of 2002 (NJHOSA) sets down the guidelines for lenders in the state. This Act is designed to protect the interests of the owner, by way of several prohibitions levied on lenders. It ensures that scams like Negative Amortization and Balloon Mortgage, i.e., ones with hidden lump sum costs, are not suffered by homeowners. However, ultimately, it is the owner's responsibility to remain aware of the law or to seek out legal advice so as to prevent any fraudulent exchange. The New Jersey Department of Banking and Insurance's Guide for First Time Home-Buyers recommends that one read the contract thoroughly before signing on the dotted line.