Taking a Hard Look at Obamacare - Success or Failure?

The Patient Protection and Affordable Care Act (PPACA) more commonly called the Affordable Care Act (ACA) or, Obamacare is a United States federal statute signed into law by President Barack Obama on March 23, 2010. The law was part of an overall program by the president to reform the healthcare industry by giving all Americans access to affordable, quality health insurance and to reduce the growth in U.S. health care spending. Together with the Health Care and Education Reconciliation Act amendment, they represent the most significant regulatory overhaul of the U.S. healthcare system since the passage of Medicare and Medicaid in 1965. The bill itself is 1990 pages long, but the associated regulation and their enforcement resulted in 159 new government agencies, boards and programs and another 20,000+ pages of documentation.

The bill was passed narrowly in the House of Representatives with only one Republican voting in favor of it and 39 Democrats voting against it. The final count was 220-215 (218 were needed to pass the threshold.) Significant controversy surrounded the bill until it was passed and many people still have issues with how it’s being administered today. The aim of the law was to guarantee all citizens had access to healthcare even if they had pre-existing conditions or other reasons which made them uninsurable. The law provided subsidies for low-income families to offset out-of-pocket costs but in order to maintain its financial viability required all Americans, even young healthy people, to have insurance. The law also required businesses with over 50 full-time employees to provide company sponsored insurance. In addition, the law bans insurance companies from denying health coverage to people with pre-existing conditions and allows young people to remain on their parents' plans until age 26. Due to many dramatic changes in the system, Obamacare was scheduled to be rolled out in phases.

Rocky Start

The initial phases were immediately plagued with a host of consecutive problems which resulted in the President delaying start dates by as much as a year. These delays were positive for many people who were struggling to understand how the law impacted them, but were in fact an illegal act by the President. Refusal to enforce the guidelines of a democratically enacted law is against the Constitution. American presidents have, under Article II, Section 3, a "duty, not a discretionary power" to "take Care that the Laws be faithfully executed.” The President and his team found enough supporting evidence from past administrations following similar protocols that it became a non-issue. Some of the other issues that happened such as the main website healthcare.com crashed repeatedly and was viewed across the technology sector as un-secure, the President had to walk back his promise of “you can keep your doctor,” the site was not bi-lingual, and enrollment deadlines kept changing.

Damning Quote

“Lack of transparency is a huge political advantage, and basically, call it the stupidity of the American voter or whatever, but basically that was really, really critical for the thing to pass.”

-Jonathan Gruber, Obamacare’s architect

Supreme Court

These issues among others prompted those who were opposed to the law to launch legal challenges to the Constitutionality of the law. To date Obamacare has been challenged over fifty times and counting. Yet in one of the most anticipated decisions by the Supreme Court, the law was upheld 5-4 in 2012. The decision itself was anchored in the Federal Government’s power to levy taxes and the brief written by Chief Justice Roberts was quoted as saying, “The Affordable Care Act’s requirement that certain individuals pay a financial penalty for not obtaining health insurance may reasonably be characterized as a tax,” and “because the Constitution permits such a tax, it is not our role to forbid it, or to pass upon its wisdom or fairness.” Although the law stood, several provisions of the regulatory sections were struck down as being over-reach of power but mostly it remained intact.

Doomed from the Start?

Congress has held nearly 60 votes to repeal the law, but with President Obama still the sitting President, these are considered symbolic at best. The reasons for the continued challenges, from the Republican perspective are financial among others. With billions of taxpayer dollars spent at the Federal level alone, the state co-ops still continue to fold. Experts say the co-ops failed because of artificially low premiums, strict regulations, and too many people requiring payouts. There is simply not enough money coming into the co-ops through premiums to cover the spending. Many also agree that the entire premise of the system was destined for failure from day one. Insurance companies that agreed to participate could have easily recognized that an underpriced product would be unprofitable for them but most likely expected that taxpayer funds would be used to prop it up, so they played along. What American taxpayers are seeing now are rapidly rising premiums, in addition to government spending, higher deductibles, and their choices very limited.

Co-Ops Folding

The majority of co-ops in America have folded and the $1.24 billion dollars in Federal “loan” money is unrecoverable. Estimates are that as more fail, over a million citizens will lose coverage. These co-ops are the government-sponsored nonprofits that were supposed to increase competition, yet instead are causing the greatest insurance disruption in decades. If the Federal Government decides to close them, other insurers that are part of the exchange are liable for their toxic balance sheets. When an insurance company folds receivership groups called guaranty associations sell off assets with proceeds going to any pending or outstanding obligations to policyholders. Doctors or hospitals after liquidation are then transferred to all other insurers doing in-state business, proportionately based on market share. Ultimately with no assets other than policies, the taxpayers will end up on the hook for any shortcomings. It should be noted that every other co-op left aside from one has been operating at a deficit since they opened. The Obama administration is quietly letting insurers know that they will be compensated for their losses which are in the billions. These administrative fixes won’t repair the exchanges, it’s mathematically impossible.

Some Say Its Winning

Yet, those who support Obamacare have their own talking points to bring to the table mainly that more than 10 million people have gained health insurance since the law was enacted. They will also tell of how the estimated cost of Obamacare is being revised downward yearly. And that in 2015, due in part to Obamacare, health care spending grew at the slowest rate since 1960. Meanwhile, health care price inflation is at its lowest rate in 50 years. It appears that both the supporters and those opposed to the law bring strong points up. Yet some of the key elements that were critical to the program being sustainable are not being realized. Enrollment of people between 18 and 34 is far below expectations – this group is so important as it would provide much of the funding needed to support older Americans. The penalty for not enrolling is low enough that many pay it and move on. Premiums are soaring and there really isn’t an end in sight – consumers were led to believe that this law would lower their rates, when in facts it’s done just the opposite.

Planned Failure?

So now that we have high numbers of participants on the program who are pulling funding and low numbers of people who are contributing funding it appears that Obamacare is entering a death spiral from which there is no return. Despite the financial penalty being increased, people are just saying no to the plan. The system is bleeding cash at both ends and sooner or later Congress will stop the bailout funding which will finish things off. But with all of the negatives, the Democrats will continue to preach positive statistics. Yet, in retrospective, the system that Obama dismantled could have been left alone and a new program to help uninsured people could have been started for far less money and time. Instead of doing the simple, obvious thing, which would just be to insure everyone who wasn’t insured, Obamacare used a combination of regulations and subsidies to convince, coerce, drive, or nudge America into a rough single-payer system. If another democratic president gets elected, the program will see continued fall out until the government is forced to step in and “save the day.”

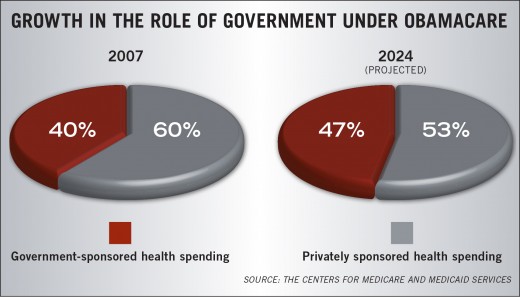

It might sound a bit outlandish but, there is a strong consensus that Obamacare was simply a planned failure to drive America in the single-payer system that Obama so loves and we see in many European nations. In this system, the government decides on the level of care a person is eligible for, what doctors can earn, and who can participate in the health industry. The theory is strongly supported by the fact that back in 2003, Obama declared himself "a proponent of a single-payer universal health care program." By the time he ran for president, he shifted to saying that single-payer was the ideal system if he were starting a system from scratch, but he acknowledged that to get anything accomplished, Democrats had to work the existing system. In 2014, according to data from the Centers for Medicare and Medicaid Services, health care spending sponsored by the federal government is projected to have risen by 10.1 percent. This was the year that Obamacare added millions of beneficiaries to Medicaid and forked over billions in subsidies for individuals to purchase insurance on government-run exchanges. If we widen our look to get a bigger picture view, we’d see that in 2007, when Obama launched his presidential run, he outlined a plan to overhaul the nation's healthcare system, private spending accounted for 60 percent of total U.S. health expenditures, compared with 40 percent coming from government-sponsored spending. By 2024, if Obamacare still exists, the government share is projected to reach 47 percent, while the private share is expected to shrink to 53 percent. With such a large shift in such a huge industry, especially when the one doing the shifting makes all the rules, it’s easy to agree with the aforementioned consensus.

Can it be Reinvented or Saved?

No matter which side of the debate you find yourself on, the fact that Obamacare only has a 37% approval rating should be telling. There are many resentful people who felt that their healthcare and preferred doctors were unceremoniously pulled away from them and they are forced to pay more for less coverage. The huge premium increases will still not cover the projected shortfalls of the program. Businesses have reduced full time workers to part time status to avoid insuring them. There are still millions of uninsured people across the country. Co-ops keep failing. About 70% of new ACA enrollees are under Medicaid, which is 100% subsidized; they essentially pay nothing to support it. Many of the remaining 30% also get some form of subsidy. A textbook view would say these collective equate a failing grade. An emotional response would say that more people are covered and that’s a good thing. A realistic view would say the program is very flawed on multiple levels but could be salvaged in a way that market-based forces are allowed to act where consumers can choose between what parts they want and understand that there are trade-offs. This will instill a sense of cost consciousness which is not seen by most people with healthcare. True market competition will require doctors and hospitals to post prices and allow for efficiencies on the provider side to drive down costs. Regulations that require insurance companies to cover everyone, similar to how it’s done with auto insurance could effectively stop anyone from being uninsurable. Subsidies from the Federal government could be used for this high risk group. The states would need to collectively agree on homogenous rules and regulations to open all providers to the entire US market. Of course, there are many more ideas on what could be done to shore up the flagging program that would be more effective with less government control, giving a win to the American people.

Summary

I'm certain that everyone has an opinion on this topic - I want to know what you think.

Keep it civil please...no hijacking the thread to start bashing the other party - the thread is about Obamacare and if its working or not.

")