To Lease or Buy?

The Automotive Blog for Independent Women...

Once upon a time, acquiring a new vehicle – be it new to you or adopted – meant one thing: buying. Not today. There are options – cash purchase, financing and leasing. And yes, depending on what model you’re considering, it is possible to lease a previously owned vehicle, though such arrangements are mostly available on high-end luxury models that retain their value.

Since cash purchases and financing are pretty straight forward, let’s focus on leasing.

Leasing Basics

What exactly is leasing? Think of it in terms of a shipboard vacation romance. You’re having fun, you’re sharing adventures, you’re getting involved – but you know there’s an expiration date on the experience. When that gangplank hits the home pier, its, “Thanks for the memories -- NEXT!”

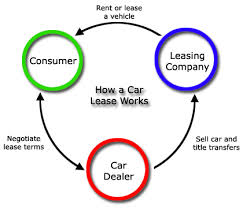

Leasing a car gives you possession of a vehicle for a set period of time, typically 24, 36, or 48 months, with some extended the use period to 60 months. Think of it as a very long-term rental. In your contract, there will be a stated date upon which you need to return the vehicle to the dealer, so, yes, you have essentially rented the vehicle from the manufacturer for a set amount of time.

But don’t even think about treating it like most people treat rental cars. That “long-time rental agreement” comes with stipulations. You can only drive 12 thousand miles a year, typically. (Some leases state 10K, others 15K so read the fine print carefully!) If you drive more than what is allowed, you will end up paying additional money for the excess mileage. Tears, a sweet smile or cleavage can’t get you out of this one. Such charges are usually 20¢ a mile, which adds up quickly. Over shoot by a thousand miles, that’s $200! But don’t even think of getting a rebate if you undershoot the mileage. Nope. Unless you love getting condescending grins, don’t even ask.

So the mistake you want to avoid is thinking you own the vehicle. You can’t treat it like it’s yours. You have to treat it like it’s someone else’s…because it is. It’s exactly like when you buy that way too expensive dress because it looks so killer on you and, hey, it’s just one night and you just have to be seen in this dress! – and then you return it three days later, after you’ve aired it out to ensure it smells fresh again. Exact same thing with a lease…only you’ve got to maintain the careful mindset for up to four years.

If you’re the type of independent woman who holds a utilitarian view of your vehicles and you prefer to be unrestricted and to go where ever you want for how ever long then leasing probably is not your best option (Note: Going across international borders with a lease vehicle is a no-no in most instances).

Given all this, is there an advantage to leasing over buying? The answer is yes – if you can live with the strings that are inherent to the relationship.

Leasing Benefits

The big advantage to leasing is you can drive a fancier, more expensive model than if you purchased. Think Louboutin as opposed to Steve Madden.

Here’s how this works -- Since leasing gives you a set time you and your car cohabit, you are only paying for the time you use it, not for the actual full value of the vehicle, as you do in a purchase. It’s like dating. You share a period of time with a man, but not his whole life. Therefore, you’re only responsible for the time you’ve spent with him…not the childhood issues that he really needs to see a shrink over.

The leasing company decides how long you’re going to use the vehicle then they determine how much the vehicle will be worth at the end of the lease period (“Residual value” is what this is called, in case you’re wondering.) They subtract the residual value from the purchase price – while adding in a profit margin/interest rate component disguised under the term “money factor” – divide by the months used and voila, that’s your monthly payment.

The residual value is why there are those stipulations on the mileage and – let’s not forget -- overall condition of the vehicle when turn-in time comes around. Gotta keep it in great shape ‘else you get penalized. (How nit-picky can it get? They even measure the size of the dings and chips in the paint. If any one surpasses the allotment for “normal wear and tear” – DING! – you’ve got another charge!) Why? Because anything beyond normal wear and tear decreases the value of the vehicle even more.

The Final Decision

So, in order for a vehicle to best fit in your life, look at it like any other relationship:

• Find one that gives you the tingles every time you see it

• Decide if it’s going to be a passing fling or a long-term commitment.

Lease the fling.

And if when that ultimate day finally arrives and you just can’t leave it at the curb where you found it… there is an out. You can always arrange to purchase the vehicle for the residual value.

Then you can totally have your way with it. Hollywood ending, anyone?

Leasing vs. Buying: The figures

So, how many folks overall opt for leasing? Current figures put the buying to leasing rates at 80%-20%.

Leasing Research Websites

- http://www.leasetrader.com

- Compare Car Lease and Auto Loan Offers - Instantly

Instantly compare car lease and auto loan offers from top lenders to get the best deal! - UsedCarLease.com new and pre owned leasing agency. Audi,Bentley,BMW,Cadillac,Corvette,Ferrari,Ford,H

Usedcarlease.com specializes in the leasing of quality pre-owned vehicles. In the market for a new or pre-owned lease visit our website. We lease Audi,Bentley,BMW,Cadillac,Chevrolet,Ferrari,Ford,Honda,Hummer,Jaguar,Land Rover,Lexus,Maserati,Mercedes