Audit Report

Public Reporting

Objective

To explain the elements of an independent auditor’ report and the expression of an opinion on financial statements.

1 BASIC PRINCIPLE

The conclusions drawn from evidence obtained (which provide the basic for the expression of an opinion) should be reviewed and assessed.

An opinion on the financial statements as a whole should be clearly expressed in writing.

Consideration:

§ The financial reporting framework (e.g. international accounting standards); and

§ Statutory requirements.

1.1 Basic elements

The basic elements are all required by standards within ISA 700.

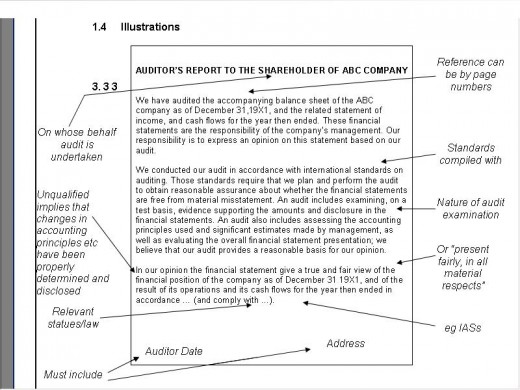

Title

Addressee

Opening or introductory paragraph

Financial statements audited

Date and period covered

Statements of responsibility

Management – for the financial statements : and

Auditor – to express an opinion.

Scope paragraph

States that the audit was conducted in accordance with ISAs or relevant national standards or practices :

States that the audit was planned and performed to obtain reasonable assurance about whether the financial statements are free of material misstatement :

Describe the audit as including :

examining evidence on a test basis:

assessing accounting principles used and significant estimates made by management :

evaluating overall financial statement presentation ;

States that the audit provides a reasonable basis for the opinion.

Opinion paragraph

“True and fair view “ (or “present fairly ,in all material respects”) in accordance with financial reporting framework ; and

Compliance with requirements of statutes or law.

Date of completion of audit, not before date financial statements are signed or approved by management.

Auditor’s address

Auditor’s signature and the firm and / or personal name of auditor.

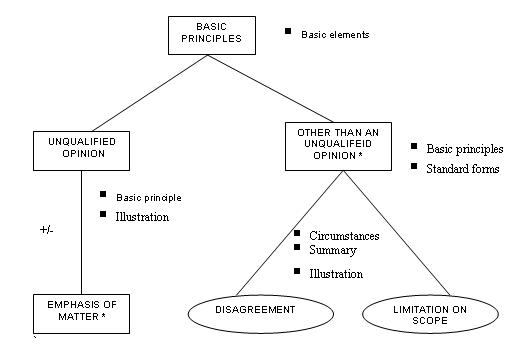

1.2 Report vs. opinion

Auditor’s report should contain a clear expression of opinion …..

That opinion may be:

Unqualified;

Other than unqualified

The report may be further modified by an emphasis of matter

UNQUALIFIED OPINION

1.3 Basic principle

When the financial statements give a true a fair view (or equivalent) in accordance with an identified financial reporting framework an unqualified opinion should be expressed.

4. EMPHASIS OF MATTER

4.1 purposes

The highlight a matter affecting the financial statements which is included in a note to the financial statements that more extensively discusses the matter.

Does NOT affect the auditor’s opinion

4.2 Form

Separate paragraph, after the opinion paragraph

Ordinary refer to fact that auditor’s opinion is not qualified in this respect.

4.3 Circumstances when used

(1) Material matter regarding a going concern problem. See Session 29.

(2) Significant uncertainty (about than a going concern problem), the resolution of which is dependant upon future events (not under direct control of entity) and which may affect the financial statements.

Illustration

“In our opinion … (remaining words are the same illustrated in the unqualified opinion paragraph above).

Without qualifying our opinion we draw attention to Note X to the financial statements. The company is the defendant in a lawsuit alleging infringement of certain patent rights and claiming royalties and punitive damages. The company has filed a counter action, and preliminary hearing and discovery proceedings on

both actions are in progress. The ultimate outcome of the matter cannot presently be determined, and no progress. The ultimate outcome of the matter cannot presently be determined, and no provision for any liability that may result has been made in the financial statements.”

§ Reference to a note is critical. If the auditor has to “make good “a lack of disclosure in the audit report must disagree with inadequate disclosure which is grounds for qualification.

(3) To report on matters other than those affecting the financial statements (e.g. concerning a material inconsistency in other information in a document containing audited financial statements)

(4) To describe additional statutory reporting responsibilities.

5 OTHER THAN UNQUALIFIED OPINIONS

5.1 Basic principles

When an opinion is other than unqualified the report should include:

A clear description or the reason; and

Qualification of possible effects, when practicable.

For a limitation on scope :

The limitation should be described:

Possible adjustments should be indicated.

A qualified or adverse opinion should be expressed for limitation disagreement with management.

5.2 Standard form

The following summaries the standards on forms of opinions and the circumferences in which each is required:

Qualified (expressed as “except for”) – a disagreement or limitation on scope is not as material and pervasive as to required an adverse opinion or disclaimer of opinion.

Disclaimer – the possible effect of a limitation on scope is so material and pervasive that sufficient evidence has not been obtained as a disclaimer of opinion.

Adverse – the effect of a disagreement is so material and pervasive that a qualification is not adequate to disclose the extent to which the financial statements are misleading or incomplete.

5.3 Circumstances

There are only two grounds for qualification:

Disagreement; and

Limitation on scope (i.e. lack of evidence reasonably expected to be available)

Not so material and pervasive

QUALIFIED OPINION “EXCEPT FOR”

“So material AND pervasive” that qualification is not adequate (financial statements misleading/incomplete)

ADVERSE

Not so material and pervasive

QUALIFICATION OPINION “EXCEPT FOR”

“So material AND pervasive” that unable to express opinion

DISCLAIMER

Imposed by circumstances (e.g. appointed after physical inventory count or inadequate accounting records)

Imposed by entity (auditor would not normally accept engagement)

Inadequate disclosure (e.g. failure to comply with relevant ISA or legislation)

Inappropriate accounting method

There is a LIMITATION ON the SCOPE of the auditor’s work

There is DISAGREEMENT with management regarding accounting policies selected or financial statement disclosures

The grounds should always be apparent because they are mutually exclusive – there must be sufficient evidence in situations for disagreement.Limitation on scope – qualified opinion

“ we have audited …

Except *as discussed in the following paragraph, we conducted our audit in accordance with ….

We did not observe the counting of the physical investment inventories as of December 31 19X1, since that date was prior to the time we were initially engaged as auditors for the company. Owing to the nature of the companies’ records, we were unable to satisfy ourselves as to inventory quantities by other audit procedures.

In our opinion, except for the effects of such adjustments, if any , as might have been determined to be necessary had we been able to satisfy ourselves as to physical inventory quantities, the financial statements give a true and ….”

*Normal usage of the word “except “

Limitation on scope – disclaimer of opinion

“We were engaged to audit the accompanying balance sheet of the ABC company as of December 31 19X1, and the related statements of income, and cash flows for the; year then ended. These financial statements are the responsibility of the company’s management. (Omit the sentence staring the responsibility of the auditor *.)

(omit or amend paragraph discussing scope of the audit according to the circumstances. Add a paragraph discussing the scope limitation as follows.)

We were not able to observe all physical inventories and confirm accounts receivable due to limitations placed on the scope of our work by the company.

Because of the significance of the matters discussed in the preceding paragraph, we do not express an opinion on the financial statements.”

* It would be nonsense to state “our responsibility is to an express opinion”

Disagreement on Accounting Policies – Inappropriate Accounting Method – Qualified Opinion

“ We have audited …

we conducted our audit in accordance with …

As discussed in note X to the financial statement, no depreciation has been provide in the financial statements which practice, in our opinion, is not in accordance with international accounting standards. The provision for the year ended December 31 19X1, should be xxx based on the straight – line method of depreciation using annual rates of 5% for the building and 20%for the equipment. Accordingly, the fixed assets should be reduced by accumulated depreciation of xxx and the loss for the year and accumulated deficit should be increased by xxx and xxx, respectively.

In our opinion, except for the effect on the financial statements of the matter referred to in the preceding paragraph, the financial statements give a true and …”

Disagreement on accounting policies – inadequate disclosure – qualified opinion

“ we have audited …

we conducted our audit in accordance with …

On January 15 19X2, the company issued debentures in the amount of xxx for the purpose of financing plant expansion. The debenture agreement restricts the payment of future cash dividends to earning after December 31 19X1. In our opinion, disclosure of this information is required by… [Reference to IASs or statute.

In our opinion, except for the omission of the information included in the preceding paragraph, the financial statements give a true and …”

Disagreement on accounting policies – inadequate disclosure – adverse opinion

“ we have audited …

we conducted our audit in accordance with …

(Paragraph discussing the disagreement).

In our opinion, because of the effects of the matters discussed in the preceding paragraph(s), the financial statements do not give a true and fair view of (or do not “present fairly”) the financial position of the company as of December 31 19X1, and of the result of its operations and its cash flows for the year then ended in accordance with … [standard] (and do not comply with … [statute]).”

")