A Beginner's Guide to Investing

In this article, you will find proven steps on how to take the money you have earned, and turn it into even more money. Investing your money for the first time can be a scary prospect. Many people don’t bother investing at all because they are unsure where to start. They equate investing in the stock market with going to a casino, and they are not sure where they can go to find the information to help them make significant investment choices. This article will help to clarify the process and give you some common-sense suggestions of how to get started. It will discuss some of the most lucrative options for first-time investors, including index funds and exchange-traded funds. It will help you to understand the risks and benefits of these funds, and how you can use them to create a diverse portfolio with a level of risk that matches your temperament. You will also learn about some higher-risk investment options such as short selling and margin trading. Once you have read this article entirely, you should have some basic knowledge about making the best investment decisions for your present – and your future.

Investing Doesn’t Have to be a Gamble

If you’re a first-time investor, the thought of sending your hard-earned money out into the world can be terrifying. You might think: it’s safe in the bank and earning interest. Why would I want to invest? You might look at film of brokers on Wall Street shouting and sweating and clutching their heads and think if professional brokers are that stressed out about investments, how can I possibly make the right choices?

It’s a natural fear to have. You work hard for your money. You may have plans to buy a home, take a family vacation, pay for your children’s college educations, and plan for retirement so you don’t want to lose all your money through investing it. We've all heard stories of stock market Cinderella. Talk about investing, and there's always someone who knows someone who bought Apple stock before anyone had heard of Steve Jobs, and is now worth millions. It’s natural to want that kind of pay-off… but what if you choose the wrong stock? What if you lose everything?

There are some basic things you can consider doing to alleviate that fear and to decrease the chances of it becoming a reality. Investing your money is a risk, but it doesn’t have to be a gamble. The best way is just to diversify your risk. Let’s use a gambling analogy to illustrate this. If you sit at the roulette table and lay all of your chips on a single number, your chances of losing everything is high. You will win only if the ball lands on the number you have picked. Not only that, but you don’t have any control over the wheel. You’re not the one spinning it, so you can’t control when it stops. In addition, you can increase the chances of you winning by betting on a group of numbers or all even or odd numbers. Betting this way reduces the size of your potential winnings but increases the likelihood that you will see some return on your money.

You can use the same principle from gambling at the casino and apply it to the stock market. If you were to buy stock for a single company and that company failed, you would lose everything. The magnificent scoop about investing is that there are multiple ways to diversify your investment, even if your knowledge of the market is very limited.

Another common fear is that watching the prices of the stock you purchase rise and fall with daily market fluctuations will be too stressful. If you’re old enough to have money to invest, chances are you’ve lived through a market downturn. Whenever the Dow Jones Industrial Average (DJIA) falls dramatically, it seems that everyone on Wall Street – even the seasoned professionals – panics. How, you may wonder, can you avoid such panic if professional stockbrokers can’t?

Again, the answer to that question is easier than you think. Stockbrokers watch the market all day, every day. If you are investing with a long-term strategy, you do not have to do that. You can ignore your investment and simply ride out short-term market fluctuations. Following this advice doesn’t mean that you should never move things around – it’s not good to be entirely unaware of what’s happening with your investments. However, if you have diversified your investment, chances are good that even if one part of your investment is underperforming others will be performing well.

Another common concern is that if you invest your money, you won’t have access to it should you need it. You can manage that fear with a little common sense. Sit down and carefully think about when you will need the money you are investing – for instant, if you have a child who will be starting college or plan on buying a home. If you anticipate that you might need the money within three to five years, you may be better off putting it in a high-yield savings account or a regular certificate of deposit (CD). If there are no particular needs for the money, you can afford to put it into longer-term investments.

Finally, many first-time investors wonder how they will be able to choose the right stocks. This particular fear is the main topic of this article. The next two chapters include in-depth explanations and analysis of two investment options that may help alleviate many of these fears and put you on track to make your first investments: index funds and exchange-traded funds.

Index Funds: What They Are, and How They Can Work for You?

Most people, even those who have never made an investment, are familiar with the Dow Jones Industrial Average. For most people, the Dow Jones is synonymous with Wall Street. We think of the Dow Jones as being the whole market. If you have never invested before, it might shock you to learn that the Dow Jones is a stock index that tracks the market performance of only thirty companies.

An index is to the stock market what a political poll is to an election cycle. No pollster would ever attempt to reach everyone in the country to find out their voting preferences. It wouldn’t be practical. Instead, they contact a sampling of voters. They try to make sure that the sample is diverse – a good mix of party affiliation, gender, age and economic status. Doing so allows them to be reasonably confident that the results of the survey are a reflection of the population as a whole. Every poll allows some margin of error, of course, but it is remarkable how accurately some polls can predict the results of elections at every level.

Index funds work the same way. The Dow Jones tracks the stocks of thirty large companies based on the price of their shares. If you purchase stock in the DJIA index fund, you are purchasing stock in every one of those companies. What that means is that you have spread your risk across those thirty companies.

The Dow Jones is only the most well-known index. There are a number of others.

The Standard & Poor 500

The S & P 500 is a large stock index tracking 500 companies chosen by the Standard & Poor Index Committee. Unlike the DJIA, the S & P 500 weighs its stocks not on stock prices, but on market capitalization. In other words, if company’s market cap is $50,000 and the total value of the index is $5,000,000, that stock would be worth 1% of the index. Most experts consider market capitalization to be a more accurate way of weighing stock values within the index.

The S & P 500 has 500 of the most widely-held companies in the country, as opposed to the DJIA, which tracks only the thirty largest companies. For this reason, many market-watchers believe the S & P 500 to be a much better barometer of the market as a whole than the DJIA. The S & P 500 follows a diverse group of companies, which makes investment in this index a potentially good choice for first-time investors.

One downside of the S & P 500 is that it is top-heavy, meaning that more than 50% of the index’s value is in the 50 biggest companies in the index. It also contains very few foreign companies, which may be a concern for some investors.

The NASDAQ Composite Index

The NASDAQ Composite Index is another well-known index. It includes every company that trades on the NASDAQ stock market, over 3,000 in all. The NASDAQ index, like the S & P 500, is capitalization-weighted. The NASDAQ index does represent excellent diversification in terms of the number of companies included. However, the NASDAQ is heavily geared toward technology companies and internet companies. There are some other industries represented, such as biotechnology and finance, but on the whole, if the technology sector is hurting, the NASDAQ will suffer as well.

The upside to investing in the NASDAQ composite index is that its contingent of technology companies represents greater growth potential than the DJIA or the S & P 500. However, the downside is that with increased growth potential comes increased risk. The NASDAQ is more volatile than many other index funds, and if the technology sector is not doing well, neither is the NASDAQ.

The Wilshire 5000 Total Market Index

The Wilshire 5000 Total Market Index tracks virtually all publicly-held companies in the United States. While its name might make you think that means it tracks 5,000 companies, the number is actually closer to 3,500 companies. Still, it represents a very broad cross-section of companies and industries, making it an excellent option for those who want a diverse investment. Like both the NASDAQ and the S & P 500 indexes, the Wilshire is market capitalization-weighted.

The downsides of investing in the Wilshire 5000 are that it is top-heavy (the top 10% of companies represent about 75% of the index’s value) and contains only companies headquartered in the United States.

The Russell 2000 Index

Unlike the other options listed here, the Russell 2000 Index tracks the performance of about 2,000 small cap companies – meaning companies with smaller market capitalization, usually between $300 million and $2 billion. Those numbers may seem large, but not when you compare them to Microsoft’s market capitalization, which is about $250 billion. The Russell 2000 is market capitalization-weighted and tracks a diverse group of companies representing most industries.

Because it tracks companies that are relatively small, the Russell 2000 can be more volatile than some of the other index funds discussed here.

Other Index Funds

The index funds discussed above are the largest in the United States, but they are by no means the only funds available. NASDAQ offers various funds that track companies for particular industries, such as finance, insurance, biotechnology, transportation and telecommunications. The DJIA offers nearly 3,600 specialized index funds, which you can review online at www.djindexes.com.

If you want to invest in companies domiciled outside of the United States, you have several options available. Most foreign countries have index funds that track stocks in their markets. Some well-known examples include the Nikkei in Japan, the FTSE 100 in the United Kingdom, DAX in Germany, and Hang Seng in Hong Kong.

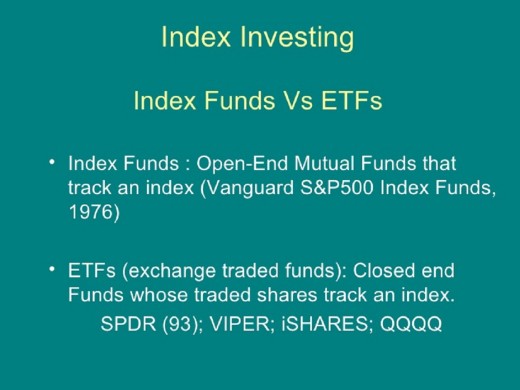

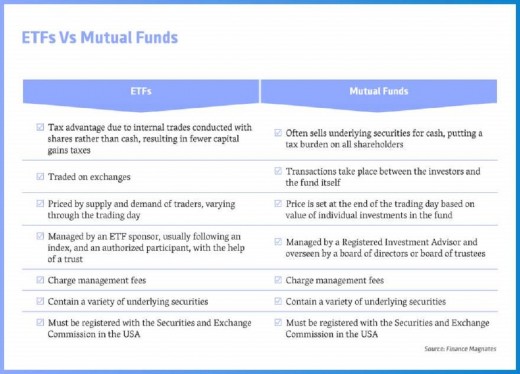

How is an index fund different from a mutual fund?

Now that you understand what an index fund is, you may be asking how it is different from a mutual fund. There are a few major differences.

1. Nobody is managing an index fund. The people who manage mutual funds take a very hands-on approach. That is not the case with stock index funds, which do not require active management. The only management needed is passive management – which means that the fund manages the weighting of the various stocks in the index based on their market value.

2. Because index funds do not require the same kind of hands-on management that mutual funds do, the costs associated with investing in an index fund are considerably lower than for investing in a mutual fund. A mutual fund might charge a 1.5% fee, which means the fund has to outperform the market by at least that much in order for you to make money. By contrast, fees for index funds average around .2%. That translates into savings for you and a greater chance that your investment will be profitable.

3. In spite of the passive management of index funds, the companies being tracked do change based on market performance. The S & P Index Committee adds and removes companies based on their performance, which means that investing in the S & P 500 is a bit like getting investment advice from the Index Committee – for free!

4. 50-80% of mutual funds fail to beat the market. Conversely, returns on the S & P 500 average about 11%. That’s a real return. Just be cognizant that you many need to ride out some market fluctuations in order to realize that kind of profit. If you panic and sell during a market downturn, you could be missing out on potential profit.

Are index funds for you?

As you can see, investing in an index fund can help to alleviate many of the fears of first-time investors, including the fear of losing everything. If you feel you have the temperament to ride out market fluctuations and leave your money in your chosen index for the long haul, investing in an index fund might be a good choice for you.

Exchange-Traded Funds

Now that you understand what an index fund is, it’s time to use that knowledge to learn about another good option for first-time investors: the exchange-traded fund. It has similarities to both traditional stock and an index fund.

How is an exchange-traded fund like an index fund?

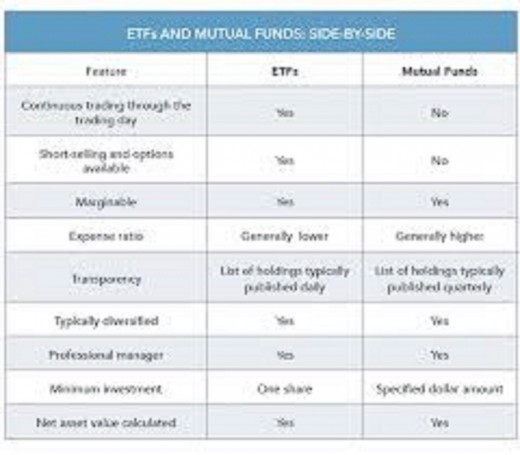

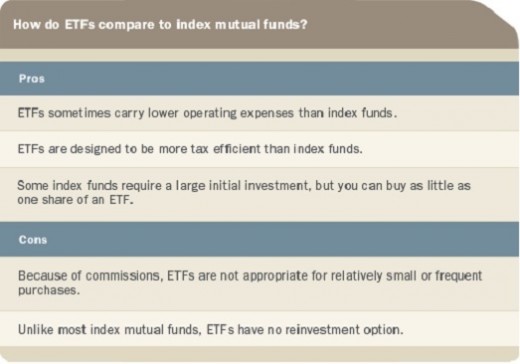

An exchange-traded fund, like an index fund, tracks an index of stocks the same way an index fund does, but its price fluctuates throughout the day like a stock. In other words, if you buy an exchange-traded fund you get the diversity of an index fund combined with the flexibility of a regular stock purchase. That means that you can sell short, buy on margin and even purchase only one share if that is your preference. Like index funds, the expense ratio for exchange-traded funds is significantly lower than for mutual funds; however, when you buy exchange-traded funds you must pay a commission for every transaction you make.

One well-known ETF, the SPDR (called Spider) tracks the S & P 500.

The upside of trading like a stock

Mutual funds adjust their prices daily. That means that everyone who buys into a mutual fund on a particular day gets the same price, regardless of same-day market fluctuations. Prices for exchange-traded funds change throughout the day based on the market performance of the stocks they track.

How can that benefit you as an investor? Well, say the S & P 500 is having an exquisite day – its value is rising rapidly. If you noticed that trend early in the day, you could buy into the SPDR, hold on to your shares until just before the markets closed for the day, and then sell them at a profit. That kind of flexibility is simply not possible with an investment in an index fund or a mutual fund. It’s riskier than buying into a mutual fund, but the potential payoff is considerably higher as well. If your tolerance for risk is fairly low, then this definitely will not be the right option for you. If you don’t mind doing a little market-watching, it can be an excellent option to turn a quick profit. Another way to explain this option is to say that it allows you to trade the entire index fund as if it were a single share of stock.

Low expenses

Another advantage of buying into an ETF is that the cost of doing so is low compared to both mutual funds and index funds. For example, the rate for buying into SPDR is 45% lower than the rate for buying into the Vanguard 500 Index Fund, which is one of the lower-priced index funds. That’s a big difference when you’re looking to stretch your investment dollars.

One potential downside of ETFs is that you will have to pay commissions for each trade you make. If you are planning to buy into an ETF for a long-term investment this probably won’t be a factor. However, if you are planning to try short-term trading, you will want to shop around for a low-priced brokerage and try to make as few purchases as you can in order to minimize your expense.

Diversifying risk

Like index funds, exchange-traded funds represent an easy method to diversify your investment and reduce the risk. There are ETFs covering every major market, including foreign markets, and covering every industry. There are hundreds of ETFs available, so with a little research, you can find an ETF that will suit your needs.

Another option that may help you to reduce your risk is a fixed-income ETF. While there are not as many options available if you go this route, you can elect short-term, mid-term or long-term bonds. Many pay dividends, and you may be able to reinvest the dividends without an additional charge. Make sure to check with your broker, because some brokerages do charge for reinvestment.

Tax benefits

In addition to flexibility, small fees, and risk diversification, investing in an exchange-traded fund can offer tax benefits as well. When you make the decision to sell ETF shares, you can roll them over into any one of the stocks the ETF tracks without having to pay taxes. What that means is that you can defer paying taxes on your profits until you are ready to cash out your investment.

Understanding Other Investment Strategies

At this point, you have a general understanding of how index funds and exchange-traded funds can help you make long-term investments. You may still have questions about terminology, especially when it comes to trading ETFs. Here are a few definitions of other investment terms to help you understand your options.

Short Selling

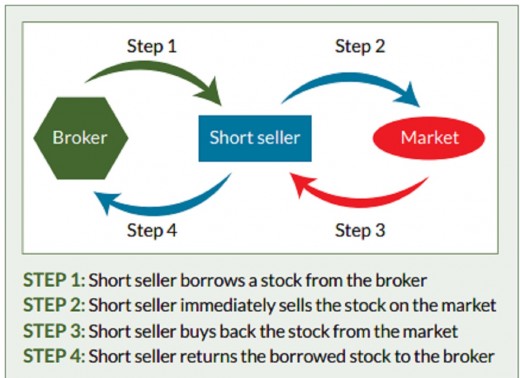

A short sale is a form of speculative investment. It involves a trader borrowing shares of stock that he does not own. He sells those shares (on behalf of the person from whom he borrowed them.) Let’s say he borrows 100 shares and sells them for $25 apiece. That means he makes $250 on the sale. If a week later the value of those shares has dropped to $20, he can buy the same hundred shares for $200, and he will have made a profit of $50.

This kind of trading is risky. If the trader doesn’t sell at the right time and the stock that he short-sold increases in value, he could end up losing money on the sale. The person who owns the stock can demand it back at any time, and he would have to purchase it back at whatever price it was trading at that day. For that reason, this type of transaction is probably not a good choice for beginning investors. However, if you get more comfortable with investing and have some money to play with, it can be a real alternative. Short selling is an option with ETFs – remember, ETFs let you trade the entire index as if it were a single stock.

Margin Trading

Simply put, margin trading is a form of trading when you borrow part of the purchase price of a stock from your broker. In order to do any margin trading, your broker will require you to open a special account called a margin account, which is essentially a deposit with your broker. The minimum amount needed to open a margin account is $2,000, but some brokers may require a higher amount.

Once you have opened your margin account, you may borrow up to 50% of the price of a stock from the broker. If you wish to purchase 100 shares of a stock trading at $50, usually, that will cost you $5,000. If you borrowed 50% from your broker, though, you could get the same number of shares for only $2,500.

Margin trading can be a good option if you are looking to make short-term investments, but it is not an especially good choice for long-term investment.

There are several reasons for this. The first is that your loan from your broker is, in fact, a loan, meaning you have to pay interest. The longer you hold on to your broker's money, the more interest you pay – and the likelihood that you will make any profit, or even break even, decreases. Another drawback to this kind of trading is that the securities you have purchased using your broker’s money act as collateral for the loan itself. What that means is that if your stock’s value drops, so does the amount of your collateral. Brokerages will require that you keep a minimum amount on deposit with them, and if the amount you have on deposit is insufficient to cover their loan to you, you may have to deposit more money. If you are not able to deposit sufficient funds, your agent may issue a margin call.

A margin call is what happens when the amount in your deposit account falls below a certain level, known as the minimum margin. Many brokerages require that the margin account is worth 25% of the value of the stock. However, some brokerages have higher limits. If the brokerage issues a margin call and you are unable to meet it, they can sell as much of your stock as they need to in order to bring the margin account to the minimum required amount. They may not even need to tell you that they are going to sell. Requirements vary from brokerage to brokerage, so you definitely want to read the fine print of your agreement with them before making this kind of investment.

The benefits of margin trading are that with the borrowed money, you have more purchasing leverage than you would on your own. That means the potential for a big payoff is higher than if you only purchased a smaller amount with your money. With that potential, though, comes a higher degree of risk. If your stock loses value, the potential exists that you could lose your whole investment and have to pay interest and fees as well. One vital thing to remember with this kind of trading is that while you may borrow up to 50% of the stock’s price from you broker, you do not have to borrow that much. If the risky nature of this type of trading intrigues you, but you still want to exercise caution, you can do that by borrowing a smaller amount. If you borrow only 10% of the purchase price, you are still getting some additional leverage but without as much risk. In short, margin trading can be a good short-term strategy, but it is riskier than investing in a fund and probably not for the novice investor.

Dividends

A dividend is simply a share of company profits. Usually, the board of directors will decide how much of the profit to distribute to shareholders. Smaller companies, or companies that are growing quickly, may choose to reinvest dividends instead of paying them out. Larger, more stable companies do pay dividends to their shareholders. If you want to have dividend income as part of your portfolio, you will want to invest in things like the S & P 500. While the benefits of a small purchase will not bring you much income, it can be gratifying to see some return on your investment without having to sell your stock. Receiving dividends can help to alleviate some of the stress associated with investing.

Tips for Beginner’s Investors

I hope my article gave you some tips on ways a novice investor can understand the stock market and make smart choices. Most people think of purchasing stocks in individual companies when they think about investing in the stock market. However, armed with the basic information in this article, you now know how many more options you have available to you.

You know that the concerns you have about investing as a novice are standard – and you also know that there are ways to alleviate those fears. You know that you can diversify your investment and reduce your risk, and you’ve learned some strategies to help you ride out market fluctuations.

You know that you can easily diversify your investment – and minimize risk – by buying shares in an index fund instead of in a single company. You have basic information about several of the largest index funds available. You understand why purchasing shares in an index fund is a safer option than investing in a single company. Index funds allow you to spread your investment over a large number of companies and take advantage of the stability of the market as a whole.

You know that exchange-traded funds give you the stability of an index fund combined with the flexibility of an individual stock purchase. You understand why exchange-traded funds and index funds charge lower fees than mutual funds, and how that can benefit you. You know a little bit about some of the trading strategies you can use with both ETFs and individual stock purchases. If you want to learn a little more about the risks and rewards concerning short selling and margin trading, then reading this article will guide you. You have the simple tools you need to make decisions about whether you can tolerate the higher level of risk intrinsic in these transactions.

In short, you are ready to get out there and start investing. Remember, the key here is to, for the most part, take a long-term view of things. If you think you will need some of your money in the next several years, do not invest it in an index fund or an ETF. Put that money into a high-yield savings account or a CD – and remember that with a CD, you will be required to pay a penalty in the event that you need to withdraw your money early. Be prepared to ignore your investment as necessary to avoid the stress of watching daily market fluctuations. Just because the brokers on Wall Street are panicking, that doesn’t mean you have to panic as well.

We all want to own homes, send our children to college and plan for retirement. Realistically speaking, the only way most of us can do that is by putting our money to work for us. Making that a first investment can be intimidating, but it can also be very empowering. When you invest your money, you take control of your future.

Now that you have the information you will need in order to start investing, the next step is to research index funds and ETFs and decide which of these investment options is best for you. It’s a good idea to take the time you need to pick an investment that will strike the right balance between potential returns and potential risk. You will need to evaluate the options and decide how much risk is acceptable for you. If you pay attention to the best stocks to buy and utilize the guidelines outlined in this article, you will be fully on your way to making smart investments. Making those investments can help to secure a bright future for you and your family.

Rate this article

© 2014 Mae Merriweather aka Boss Lady Mae

System for Timing the Stock Market")