Budgeting Tips for the New Year!

Budgeting Tips for the New Year!

Well it is the first day of a new year and it is time to do the budget. For some reason, I have always loved budgets because I can get more out of my money this way. While many will budget with an income in mind, I have to do my budget a little differently. As a freelancer, my income is ever changing, so m budget is for what needs to be paid and regular expenses, as well as a slush fund for the annual expenses that come up in life. Any money left over will go mainly to savings with a percentage going into slush fund for unexpected purchases and a small percentage goes to mad money.

I will share below my real 2018. I don’t know how much I will make this year, however I would considered a lower income for a family of four, however I make it work for me by living in a lost cost area where my money is able to stretch.

Getting Started.

If you are new to budgeting, it would be good to know what the average amounts are that you spend in any given month. This will give you a starting off point and I like to go back and look at my expenses for the last 1-3 months. If you don’t keep up with your expenses, try using your debit card to go through your charges to get a realistic idea of what you actually need for each category.

Write down what kind of things you need money for. Bills are a given, but you need to write down all of your other categories you can think of.

Monthly Expenses and Categories:

Water, Sewer, Electric, Rent, Internet, Phone, Cable, Natural Gas, Medical premiums, etc.

Household Running: Food, Household items, Baby, Kids, yard maintenance

Savings

Next Step, Annual Costs:

When you have all of your categories for your monthly expenses, I like to go through and fill in my amounts for annual charges like car insurance that I pay twice a year. While many people would call these costs sinking funds, I throw it all together and call it a slush fund. Unless you are a year ahead, the amount is not there to the end of the year, so I like to keep it together for a better chance to have what I need, when I need it.

Try to think about all of those things that you need throughout the year. This could be anything from tags on your car, annual or bi-annual insurance costs, medical costs that aren’t in your premium, like deductibles, vacations, school supplies, whatever you need throughout the year to keep you going that isn’t a normal monthly expense. It is good to get a jump on these things because Christmas and birthdays come every year, so it shouldn’t be a big surprise.

With a little forethought, you can take the stress out of these ‘surprises’ because you will have the money set aside to keep you going and you won’t be scrambling to find the money or dipping into an emergency fund. It is also good to think about common costs like car maintenance because you will need to put some money into your car throughout the year. If you have pets, set aside a bit for the veterinarian and other costs associated with owning a pet beyond food, like flea and heart worm medicine, check-ups, things like that.

Now put the numbers in place and see where you are.

For me, I do this backwards. I don’t know how much I am going to make. I more or less come up with a target amount that I have to make per month to keep us living comfortably. If your number is too high, you have to get more realistic and either cut costs and bills or find a way to make more by supplementing your income. You can’t spend more than you make.

If I don’t hit my target, I order my budget in priorities first and go as far as I can down the list. If I don’t have enough to pay everything, rent and bills, food, etc., get paid before savings and slush fund is funded. I have no debt; paid it all off last year, but this would be a lower priority. You have to keep your house going and your car running before you pay on credit cards. Some items can be cut and if I am having a short month, I will go into pantry challenge mode and half my grocery bill for the month. Many items on your budget are discretionary and can be lowered if needed.

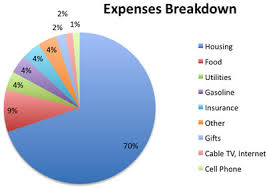

My 2018 Budget for a family of 4

Monthly Expenses

Rent: 600

Water: 50

Sewer: 50

Electric: 75

Frontier: (Internet and Phone) 75

Natural Gas: 50

Netflix: 20

Food: 150 (for eating out as well. Works out to 25/wk. fresh and 50 a month on pantry, formula and sale items. To save on formula, contact the major brands and ask for coupons, they will provide hundreds in savings by just asking.)

Household: 50 (TP, shampoo, soap, detergent, etc.)

Baby Ophelia: 50 (diapers and whatever is needed)

Shane: 50 (days out, any extras)

Gasoline: 80

Misc.: 100 (mad money or anything needed that pops up and not included in slush fund)

Medical: 200 (medication and co-pays)

Medical Premiums: 500

Slush Fund: 200

Savings: 500

Target: 2800

Additions:

May-October Yard Maintenance: 120 (2920)

November-February Heating: 100 (2900)

Slush Fund- Annual Costs

Homeschool: 150 (Standard curriculum, fill-ins, portfolio review)

Christmas: 400

Holidays: 50

Clothes: 200

Birthday: 300

Car Insurance: 600

Car TTL: 200 (car tags, license renewal, etc.)

Vacation: 500 (one week in summer)

After target, 50% to savings, 25% to slush fund and 25% to mad money.

That’s it. I keep many prices low by shopping sales throughout the year. I do rebates through Ibotta, credit card rewards by purchasing most things and paying bills with credit card and reaping rewards for gift cards throughout the year. Food costs are low here and with a well-stocked pantry, I never buy anything that is not on sale, ever. Clothing is bought in offseason for following year. With a little forethought, most costs can be halved or better.

Is your budget ready for the New Year?