How to Protect your Unemployment Benefits from Creditors

Although each state may be slightly different in what they allow creditors to do, it will pretty much follow along the same lines as those here in Michigan. Before relying on this information, please check with your state unemployment office.

When you file for unemployment, you are given the choice of two payment options: A debit card or an automatic deposit into your checking or savings account. Many of us do not realize the importance of this decision and the ramifications of the wrong choice.

When creditors are after you for nonpayment of credit card bills, they can and will use legal means to get your money. It may take some time and depending on the amount that you owe, they could be ruthless about it.

It starts with the phone calls. Unrelenting phone calls to be precise. They will call you every day whether you talk to them or not. You can be nice and explain the situation, which most people do at the beginning, or you can either screen the calls or ignore then and turn off your phone. But they will continue to call. Do not give them information. Everything you say can and will be used against you. For more on creditors calling, please read - Are Creditors Calling you?

When the phone calls do not produce the desired results, they may take further action, without much notice. One of the initial steps that your creditors may take is getting a judgment against you. They will file papers with the court in your home town. You are not required to be there unless you intend to fight this action. However, you must be notified. Unless you can show reasons why you do NOT owe the money, they will get their judgment. This judgment states only that the court acknowledges that you do owe the money. For most of the unemployed, it isn’t a matter of whether you owe the money or not, but simply the inability to pay. It is what they can do, by law, with this judgment that you really need to be concerned with.

With a judgment against you, creditors can seize the money in your bank account. They must file a request for garnishment with the court but if they have that judgment, this is only a formality. When you are employed, a creditor may garnish your wages by filing court papers to the company that employs you. When you are collecting unemployment benefits, the court papers are filed to the bank that holds your money. The bank has no choice but to comply. They will also send you notification. Once your creditor files this garnishment, the money in ALL of your accounts can be frozen: you can’t touch it, pay bills with it or withdraw it. Your creditor cannot have it at this point either, yet. You are sent a copy of the garnishment paper by the court. You have 14 days to file objections with the court.

This is where state law may differ. This report is on what happens in Michigan, but like I said before, the laws will be similar, so check with your local courts.

A creditor may not garnish your unemployment from the state itself; they must wait till you have custody of the money. Your custody begins the minute that money hits your account. The freezing of your account may happen without your actual knowledge which can really get complicated if you have recently written checks or paid bills online. You will be held responsible for any overdrafts and the fees that accompany them. And of course there will be a legal processing fee charged to your account for the garnishment.

The steps I have outlined above can be further complicated if accounts are held jointly or if Social Security deposits are involved. All Social Security money is exempt from garnishment. But in a joint account, what money is whose, is up for grabs.

Within the 14 days, you may file an objection if you can clearly show that the money in your account comes from unemployment benefits. Some judges may protect this money from creditors, but case law is not clearly spelled out due to the new paperless aspect of paying the benefit. The money is no longer a check mailed to the recipient. It is automatically deposited. This gives the creditors a crack at it before you can get your bills paid. I’d love to be able to tell you that unemployment benefits are exempt from garnishment but it isn’t clear. So protection is needed. The best way to keep creditors from seizing the money in your bank account is to not have any money in your account.

At this point, any other non-exempt money in your account can and will be given to the creditor. The bank’s legal department or the court clerk may be able to answer some questions for you. As a side note here, if you have real assets that are in danger of confiscation, you should call a lawyer before your 14 days are up. Be aware that any property your own that does not have a lien on it is up for grabs to any creditor with a judgment. For example, if you own a car outright, any creditor with a judgment may repossess that car even though the car is paid for. This holds true for any property that you may own.

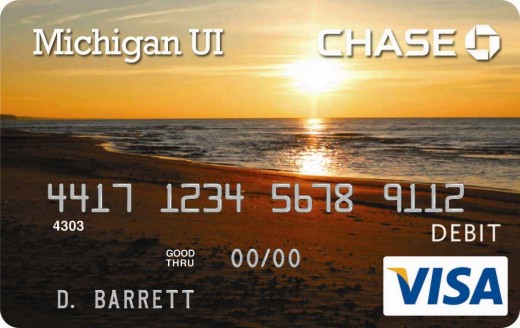

If you have a judgment against you and you are collecting unemployment benefits, you might need to consider changing your payment option to the debit card. If you have chosen the debit card option all of the above can still hold true but your money is in your hands and not in the bank.

In order to facilitate payment of benefits, the state will enter into an agreement with one or more banks to act as a clearing house for unemployment benefits to be paid by debit cards. Here, in Michigan, Chase Bank is the bank that issues the debit card. This debit card alone does not grant you access to any of Chase’s account privileges because the issuance of this debit card does not make you a Chase customer.

Now I don’t know what is like for those in other states, dealing with other banks, but here, Chase will only allow you a limited amount of services free of charge. There are a myriad of services that they will charge you for including a fee to withdraw money from the card more than one time per deposit. So be sure to read the details that accompany your debit card.

For those that enjoy the convenience of paying their bills online, that option has just become a veritable game of chance through any bank because the minute you deposit the funds to pay your bills they can be frozen by a new garnishment. Starting a new account in a new bank will only hold them off until they run another credit check on you - and they will find you.

Ok, so now we have our debit card with 2 weeks of unemployment benefits loaded into the card. You are able to use that card, without any fees, for your purchases anywhere that accept credit cards. But when it comes time to pay your bills with the money on the card, you have to rethink things. You cannot use your account to pay them, either by online bill pay or by writing checks. The money in your account won’t be safe sitting in there waiting for the checks to clear. It simply isn’t worth the risk.

Not everyone will be able to pay all of their existing bills on unemployment alone. For a better understanding of what bills absolutely need to be paid and what bills don’t belong in that need category, read – Unemployed and Can’t Pay Your Bills?

You have a few options. You can go to the website of the company that you owe the money to. Often you can pay by debit card right there. Although, some restrictions may apply so read all of the instructions and the service agreement. If you choose this option, very often the company may stop sending you a paper bill in the mail each month choosing instead to send the bill electronically. If this is not acceptable to you, then you may have to find another means to pay your bills.

Another option that companies often offer is to pay your bill over the phone using your debit card. However, this is an expensive avenue to choose. Each transaction will be charged a fee. These fees can range from $3 to $15 per transaction and can really add up fast. This is not a sensible solution when money is tight while trying to live on unemployment.

The last option is withdrawing all of the money from the debit card, purchasing money orders and sending in the payment the old fashioned way – by mail. Remember that multiple withdrawals from a single deposit can incur fees so if you choose this option, it might be best to withdraw all of the money out right away. If you choose to keep some money on the card, you can have the peace of mind that because this is not an actual bank account; your creditors will not have access to this money. When it comes to purchasing money orders, very often your personal bank will issue money orders without charge so be sure and check there first. Otherwise, call around, the price of money orders really fluctuate from store to store.

Second guessing what creditors may or may not do, can be a full time job in itself. Protect yourself. The bottom line is that if your creditor has a judgment against you, your money is not safe in the bank. This doesn’t stop at just your checking account. All of your accounts are possibly fair game, savings, college funds, and even money market accounts.

Your income tax return is also fair game for a creditor with a judgment against you. They will probably confiscate your refund as well as tap any other recurring settlement checks you may be receiving. You may need to contact a lawyer is you believe that your recurring settlement money should be exempt.

If you have questions, you need to speak to your bank representative. The bank teller may not be able to answer all of your questions so don’t hesitate to talk to the bank manager. If the manager is unable to answer your question the bank’s legal department will be able to help you.