Insurance: Fear and Loathing

Do You Dread Calling Your Agent?

Insurance Is So Confusing!

Is dealing with auto insurance something you dread? Do you feel slightly intimidated by your insurance agent because you have driving record issues? As a longtime agency owner, the first thing I’d advise is that you immediately shop for a new agent.

You should never dread calling your agent and asking whatever questions you have about your coverage, your driving record, or your rates.

That said, there are some basic tips that will help your agent serve you better. Generally speaking, your agent wants you as a customer even if you have a crummy driving record. Agents don’t judge you but they understand that your rates will be partly based on how you drive and most good agents want to offer you the most competitive (least expensive) coverage possible.

Accidents Happen

There are limits here though and if you have several accidents where the insurance company must pay many thousands of dollars in auto repairs and liability (lawsuits) because of your driving habits, your agent may advise you to find coverage elsewhere. Having several customers who have many costly accidents damages the agent’s relationship with the insurance carriers (companies).

Sample Cost of Vehicle Crash

Cost to replace 2009 Explorer

| $16.000.00

|

|---|---|

Medical cost for minor injury

| $4500.00

|

Cost to repair other property

| $4700.00

|

Total cost for one accident

| $25,200.00

|

Average annual premium for one car

| $800.00

|

total cost to insurance company

| $24,400.00

|

Insurance Companies Are Just Greedy!

I hear it all the time, “All you do is collect money for my premium and make the insurance company rich!” To be sure, insurance companies are for profit businesses. They are not charities. Their success is dependent on attracting the greatest number customers who will not cause them to lose more money than they collect in premiums. Insuring too many risky drivers puts the insurance carriers in danger of not having enough money pooled to cover costly accidents or catastrophes.

Each insurance company is regulated by the State Insurance Commission as to how much money is kept ‘in reserve’ to cover losses (accidents, lawsuits).

Who Is At Risk?

It is important to understand that when an insurance company insures (provides a policy to) an individual, the financial risk is much greater for the insurance company. Most people are good drivers but accidents occasionally happen to almost every driver. The risk for the insurance company is that a driver may pay a few hundred dollars to a company in monthly premiums and then have a devastating accident. The insurance company will then pay for auto repairs for the customer’s vehicle, the damage the customer caused to other vehicles or property, medical costs for the customer and possibly defend the customer in a lawsuit that may cost many thousands of dollars. Simple math reveals that the insurance company may lose substantial money on this one customer.

In a large insurance company with hundreds of thousands of customers, one customer having an expensive accident does not impact profit or deplete reserves. However, with hundreds of thousands of customers, several thousands of those customers have accidents every day. That adds up to millions of dollars being paid out for repairs and lawsuits and cuts deeply into the insurance company’s ability to cover other losses. When choosing an insurance company, drivers should look for companies which maintain high profits and reserves.

Insurance Companies Have Plenty of Money!

Even if you have paid premiums on a policy for several years... let’s say at an average rate of $800.00 a year for one vehicle and you have an accident five years into the policy, you have paid in roughly $4,000.00 in premiums. If you total (completely destroy) a newer vehicle and damage another vehicle and maybe cause at least one person in your vehicle to be treated by a doctor, the cost of that one accident may be as much as $20,000.00, and that is a very conservative estimate. This very rough example and does not accurately account for the cost to replace a five-year-old vehicle, costs to repair another vehicle and leaves out entirely the possibility of you being sued by the other driver.

The actual cost to cover this accident may be thousands of dollars more. Or less, depending on the severity of the accident. My example here is only to point out that the risk is on the insurance carrier, and even after collecting premiums from you for a few years, there is a substantial possibility that your one accident will cause a loss for the insurance company.

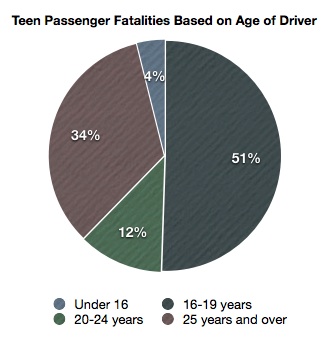

Frightening Statistics

- 2009 Statistics for US Auto Crashes

This shows some of the breakdown of car crashes in the US.

I’m a Risk???

Underwriting guidelines are used by each company to assess the risk of all applicants. Customers have to fit somewhere in the guidelines to be accepted into the insurance pool (group of similar drivers, often called a tier).

When a vehicle owner applies for insurance coverage, several criteria are used to rate the driver's risk, including driving records, driving experience (age and length of time licensed), gender, zip code, credit rating and insurance score, which is a combination of all the above plus the length of time in the most recent insurance policy. Other factors may be used by insurance companies but be assured that all applicants are rated using the exact same criteria. Also considered are marital status and the presence of young drivers in the home. This is called underwriting.

It's All About The Numbers

All of the criteria used in rating a risk is based on statistics. For instance, people who have had a speeding ticket are more likely to have another speeding ticket, so the rate is based on that probability. Folks who have had accidents may be more likely to have more accidents, either because they are unlucky or because they are not the best defensive drivers. Young, single, male drivers have the highest rate of serious accidents than any other group--combined. So, rates for those drivers are higher than rates for slightly older married men who have had no accidents in the last three years. It’s all about statistics.

Some of the underwriting guidelines are based on the driver's behavior, such as whether or not the driver has a college degree, has good or bad credit, has tickets or accidents in the last three years, has maintained previous insurance policies for an adequate length of time, has driven without insurance for any length of time, how many miles the vehicle is driven each year and many more factors.

Other rating factors include basic costs to repair vehicles in a certain zip code or area, the statistics of accidents and comprehensive claims (theft, fire, hail) in a zip code, and the actual vehicle itself, including safety features such as anti-lock brakes, airbags, alarm systems, etc.

All of the underwriting criteria is combined to rate the risk, that is, determine the cost of the premium for a driver and a vehicle.

Don’t Be Intimidated—Be Prepared

That’s a lot of information for the average reader who just wants to find a more comfortable way to deal with auto insurance. There are ways to approach your agent and handle your insurance needs without the fear and dread that many people feel, especially folks with bumpy driving records and a recent history of bad luck behind the wheel. Remember, your agent is a human being first and a business owner second. S/he also drives and may have kids and struggles with the same daily stresses you do.

I strongly recommend using an agent as opposed to an 800 number for help with insurance policies. Chances are good your agent lives close to you, giving her a better understanding of the unique driving conditions and costs that you face. If you have a serious accident, it may be more comforting to speak to a neighbor than a call center agent in a different country. Using an insurance agent DOES NOT increase the cost of your insurance premium.

Using an independent agent offers advantages as well. If you are with an exclusive company, one that only offers insurance from one carrier, such as State Farm, Allstate, Farmers, etc., you are stuck with whatever rate increases are passed on to you. An independent agent is able to shop for the best rates for you with many different carriers.

When you are ready to get a quote for a new vehicle, are thinking about getting insurance from a different company, or simply want to ask questions about your existing policy, be prepared before you make the call or visit. One of my least favorite phone calls is from an applicant or customer who calls me using a cell phone while they are driving. Besides being dangerous, they are rarely ready to take notes on premium comparisons and cannot safely read their driver’s license information to me while driving. Just don’t do it.

- What impacts my Auto Insurance price?

Advice from a licensed insurance agent.

Don't Call From Your Car!

Try these tips to make your next insurance phone call or visit more satisfying :

Collect the information you need before the call:

Policy number

Driver’s license numbers

Social security numbers

Year/make/model of vehicles

Vin number of vehicles

Mileage of vehicles

Prior policy number (when getting a new quote)

- Don’t call unless you have at least twenty minutes of uninterrupted time.

- Don’t call while driving a car.

- Be prepared to give out sensitive information to get a ‘firm’ quote as opposed to an estimate.

- Be honest about your driving record. Your quote will be miscalculated if you ‘forget’ accidents or tickets you’ve had in the last three years.

- If you get what you perceive as bad customer service on the first phone call, try another agent.

- Use an independent agent to get quotes from several different insurance companies rather than making several calls to agencies which only offer one carrier.

- Have a notepad and pen ready to write figures for comparison

- Most people find it convenient to give out email addresses to receive the quote

Your agent should treat you with respect and building a relationship with her/him is a good way to make sure you feel comfortable discussing your insurance. If you feel uncomfortable discussing your questions and concerns with your agent, find a new agent.

© 2014 bzirkone