Retirement Savings Options for Small Businesses and the Self-Employed

Money earned from small businesses or self-employment can be saved for retirement.

Small business owners, entrepreneurs, independent contractors, free-lancers, bloggers and even Huggers can earn money, from small sums to large, through self-employment. After expenses are paid, the net income from self-employment can be used as a primary source of income, a little pocket money, or to supplement your retirement income.

Don't have a retirement plan? Your retirement savings a little short? Business income can be used to fund a retirement plan of your own.

There are several options for retirement plans for the self-employed and small businesses. They all have their advantages and disadvantages. Some defined contribution plans are low cost and easy to set up and administer. The key is to find the right plan for you and your business.

Keogh's and defined benefit plans, while potential options for small business owners,particularly those with high incomes, are more complex, more costly to set up and maintain, and won't be discussed here.

Some questions to consider before you choose a retirement plan for your business:

- Do you also have a job as an employee at a business with its own retirement plan? Do you participate?

- After expenses, is your net income from your business large or a small?

- Do you have employees or are you a sole proprietor?

- Do you want the plan to include your employees?

- Are you over age 50 and want to take advantage of the catch-up option?

Table of Contents

Retirement Plans for Everyone

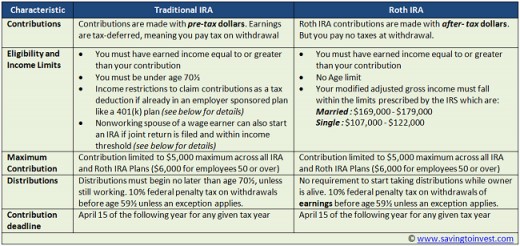

Traditional IRA

Anyone with earned income can contribute to a traditional IRA up to a maximum of 100% of their income, but not more than $5,500 ($6,500 if over age 50) for 2018. A contribution can be made for an unemployed spouse if one spouse has earned income (spousal IRA).

Advantages:

- Easy and inexpensive to set up

- If employer allows, can arrange for payroll deduction

- Do not have to contribute to every year.

- Contributions may be tax-deductible for certain taxpayers.

- Depending on where the account is set up, investing options may almost be unlimited and can include: savings accounts, CDs, bonds, stocks, mutual funds, and ETFs.

Disadvantages:

- Withdrawals are taxable as regular income and withdrawals before age 59 1/2 are often subject to a 10% penalty.

- For higher income individuals, contributions are often not tax deductible.

Roth IRA

Rules are much the same as the traditional IRA, but the contribution is not deductible (but it grows tax-free). There are income limitations with regard to who can contribute. Even if your income exceeds the limits to contribute directly to a Roth IRA, you can still contribute to a traditional IRA and then convert it to a Roth IRA (this was a change in the rules in 2010). You must have the Roth IRA account for at least 5 years and exceed age 59 1/2 before making a withdrawal or taxes and penalties will be applied (exceptions include buying a first house, death, or disability).

Advantages:

- Contributions grow tax-free and withdrawals are not taxable.

- No mandatory minimum required withdrawal after age 70 1/1.

- Can pass the account on to your beneficiaries and they continue to enjoy the tax-free growth and withdrawals.

- Contributions can be withdrawn any time.

- You can contribute any year you have earned income regardless of your age (other rules apply).

Disadvantages:

- Contributions are not tax deductible.

- Contributions are limited by your income.

- If you exceed the limits, contributing is more complex and requires a conversion from a traditional IRA. For a conversion, tax will be owed on both the growth and any deductible contributions made to the traditional IRA. Non-deductible contributions will not be taxed again.

Note: Table for 2011 contributions. Contribution limits for 2018 are $5,500 ($6,500 if over age 50). Phase out amounts for Roth IRAs for 2018 are $189,000-$198,999 (9MFJ) and $120,000-$134,999 (Single).

Traditional IRA versus Roth IRA Comparison (2011 Amounts)

Individual or Solo 401(k)

Available to self-employed individuals or business owners with no other employees (except for possibly the spouse of the sole proprietor). An individual or solo 401(k) is just like a regular 401(k) established by a larger business. It is available in a traditional (deductible with taxable withdrawals) option or a Roth (non-deductible with tax-free withdrawals) option.

Advantages:

-

Ability to save a larger amount money because of a greater limit on deductible contributions for smaller businesses.

-

3 components make up the annual contributions to individual or solo 401(k):

-

Maximum Employee contribution for 2018: a sole proprietor can make an employee contribution up to a maximum of $18,500 (up to a 100% of net earnings).

-

Catch-up contribution: Owners over age 50 can make a catch-up contribution of an additional $6000 of net earnings.

-

Employer profit-sharing or match: An contribution can be made of up to 20-25% on net earnings (to a net earnings maximum of $255,000).

-

Maximum total annual contribution is $55,000 for 2018 ($61,000 with catch-up).

-

Maybe the best option if you want to save $30,000 or more annually.

-

Fewer complicated government rules compared to a regular 401(k).

-

Set-up and annual fees can be low. Some custodians such as Vanguard and Fidelity charge no set-up fees.

-

Contributions are optional, so in leaner years less or no contribution needs to be made to the plan.

-

Some custodians may allow penalty-free loans.

Disadvantages:

-

May not be the best option if you also an employee and participate in your employer's retirement plan. For 2018 there is a combined $18,500/$6,000 employee contribution limit to 401(k) plans no matter how many jobs (and their retirement plans) you participate in.

-

Have to begin filing a Form 5500 report once the balance of the plan exceeds $250,000. There are reasons you may want to start filing this form with an even lower plan balance.

-

Withdrawals made before age 59 1/2 incur a 10% early withdrawal penalty plus tax on all withdrawn funds made with deductible contributions.

SIMPLE IRA (Savings Incentive Match Plan for Employees IRA

A retirement planned designed for self-employed individuals or small businesses with only a few employees (less than 100).

SIMPLE IRAs can involve a contribution from both the employee and the employer.

For 2018, the employee may contribute up to $12,500, with a catch-up contribution allowed for employees over age 50 (up to $3,000 for 2018).

Employers either:

1. Match employee contributions dollar for dollar up to 3% of employee's compensation (can be reduced as low as 1% in any 2 out of 5 years).

2. Contribute up to 2% of each eligible employee's compensation, up to $5,500 regardless of whether or not the employee contributes (Employee compensation up to $275,000).

3. Employer must contribute.

4. Must be offered to all employees over age 21 who:

- Have been employed by the business 3 our of the last 5 years AND who are reasonably expected to earn at least $5000 in a year (for 2018).

- Employee chooses to contribute and does not have to contribute every year.

Advantages:

- Easy to set-up, but a little more cumbersome to maintain.

- Offers a catch-up provision for employees over age 50 who wish to contribute more.

- Employer and employee contributions are 100% vested immediately.

- Employee and employer contributions are tax-deductible.

- May allow contributions of up to 100% of income.

Disadvantages:

- Requires an employer contribution every year. It maybe difficult for the employer to contribute if business income fluctuates year to year, particularly in the early years of a business start-up.

- Withdrawals are subject to federal income taxes and if younger than age 59 1/2, subject to a 25% penalty if taken within the first 2 years of participation and 10% if taken thereafter.

- Employees (including owner-employee) cannot contribute if they have already maxed out their employee contributions at another job.

- Maximum contributions are less than in a 401(k).

- No Roth or loan options.

Simplified Employee Pension Plans (SEP-IRA)

Simplified Employee Pension Plans (SEPs) allow employers to set aside money in retirement accounts for themselves and their employees. Contributions are made by the employer directly to a SEP-IRA for each employee (including the employer).

Eligible employees must be:

-

21 years of age

-

Performed service for you in at least 3 of the last 5 years

-

All eligible employees must participate in the plan (includes part-time and seasonal employees and employees who die during the year).

-

Do not have to include employees who receive less than $600 in compensation for the year.

Advantages:

-

Suitable for sole proprietors, partnerships, and corporations (including S corps.).

-

Little or no start-up and operating costs.

-

May allow for higher contribution limits (up to 20% of each employee's pay or 25% if incorporated). Maximum contribution of $55,000 in 2018.

-

Immediate vesting.

-

Contributions can change year to year and you do not have to make a contribution every year.

-

SEP contributions are tax-deductible to the business.

-

Usually, no documents to file with the government.

Disadvantages:

-

Must include all employees. Cannot limit to just employee-owners.

-

No Roth option.

-

Must contribute the same contribution percentage to all eligible employees.

-

Withdrawals made before age 59 1/2 are subject to a 10% penalty. All withdrawals are taxable. Mandatory withdrawals after age 70 1/2.

-

Do not allow for employee or catch-up contributions.

-

Loans are not an option.

Final Thoughts

Retirement plans for small businesses and the self-employed can be a very complex and confusing subject particularly if it involves an individual that is both an employee with another company and self-employed. If this individual was contributing a significant amount to his employer's retirement plan, the question is, would it be best for him to contribute more, if possible, to the employer's plan or to start a plan for his business? Complex situations such as this require a detailed discussion with an accountant, lawyer, and financial adviser.

Recently, there has been more interest in self-directed IRAs. These retirement vehicles have custodians that allow more unusual (but not prohibited) transactions such as investments in private placements, small business loans, small business start-ups, and investment real estate.

For a explanation and discussion of defined benefit and defined contribution pension plans, check out this hub.

Self-directed IRAs and defined benefit plans may be options for some small business owners.

Disclaimer:

Any federal tax, tax planning, business planning, or financial planning information provided above or linked to this article is not meant to be specific to any particular individual, business, or situation. Anyone who wishes to apply this information should first discuss it with their lawyer, financial or business planner, accountant and/or tax professional to determine the appropriateness of the information and how it specifically applies to their unique situation.

© 2012 Mark Shulkosky

Related

Effective Decision Making for Small Business Owners: A Complete Guide

The Village Framer - A Small Business Review - Small Business Saturday

Barcode Assets Tracking – Track Assets for Home Inventory and Small Businesses Using Excel

How to Start a Service Business; a Tutorial

List of Seasonal Small Business Ideas