Equilibrium Determination Under Perfect Competition Market

Introduction

Perfect competition is a market structure where large number of buyers and sellers interact with each other to buy or sell their products. Here one of the most important features or assumptions is that all products are homogenous and they are perfectly substitutable. So market will determine a price and which remains constant further any single firm cannot change it. So, the firms or sellers are price takers, they can only change the quantity of output of their sales. This hub is briefly described about how equilibrium condition is determined in a perfectly competitive market.

Equilibrium point is one where the market is in the rest. Which means the condition of both the buyers (demand) and sellers (supply) will be equal. When we observe a firm in a perfectly competitive industry, the firm can survive only when they earn profit or at least their revenue which is equal to cost. Under the perfect competition market, price curve will be a perfectly elastic one. Because sellers can adjust only their supply since the price is fixed. By assumption revenue curves (Average Revenue and Marginal Revenue) should be equals to price since price is fixed. Further cost curves will have ‘U’ shapes as explained in the traditional theory of cost.

Equilibrium on the Basis of Time

In modern economics time is a very important element. Mainly time can be classify in to two, they are

a) Short period and

b) Long period

Short period refers to a condition where there is no any possibility to change fixed or long run factors of production like land and building. So, if a firm wants to change their output they can only vary short run or variable factors like labor, power and fuel etc.

On the other side long period refers to a condition in which all the factors can change irrespective of fixed or variable inputs. The firm can vary both the inputs in accordance with their expansion and contraction requirements in output.

Short Run Equilibrium of a Firm and Industry

An industry will be in equilibrium when there is no tendency to enter new firms or exit of the existing firms. Which means all the existing firms earns normal profits only. Further an industry will be in equilibrium when the following conditions are satisfied.

i) Marginal Cost = Marginal Revenue or (MC=MR)

ii) Average Cost = Average Revenue or (AC=AR)

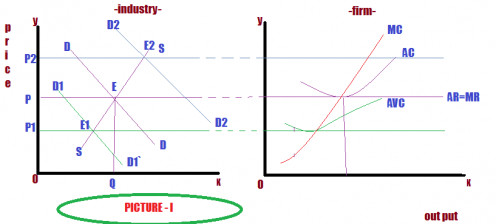

See the following PICTURE – I, which showing the equilibrium status of a firm and industry.

In a perfectly competitive market, firms are the price takers. So, market determines prices. In the above PICTURE – I represented two diagrams one for firms and the second for industry.

The industry will be in equilibrium at point ‘E’ where price is ‘P’. On the part of firms’ side at price ‘P’, Marginal Cost curve (MC) cuts Marginal Revenue curve (MR) from below and both are equal. Since, MC and MR equal at ‘F’ each firm will earn normal profits only.

Suppose at price level ‘P2’, where industry in equilibrium at point ‘E2’ and in the case of firms, at price ‘P2’ equilibrium is ‘G’, where Average Revenue (AR) is greater Average Cost (AC). So, firms will earn abnormal or super normal profits. On the other hand at price level ‘P1’, where industry in equilibrium at point ‘E1’, and the firms will be in equilibrium at point ‘H’. There AC is greater than AR, so the firms will suffer losses. The point ‘H’ is known as shut down point where AVC equals AR.

Long run Equilibrium of Firm and Industry

In long run each firms can change their inputs, both fixed and variable factors of production can be changed in accordance with their needs.

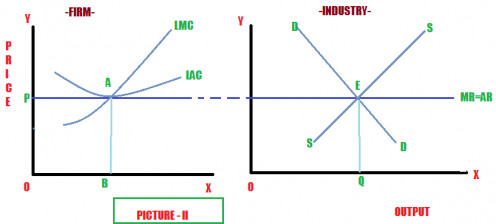

A perfect competitive industry will be in equilibrium when all individual firms are in equilibrium. Which means all firms earns normal profits. So, there is no possibility to enter a new firm to industry or exit by an existing firm from the industry. The price of output is determined by market which is common to all sellers. So, equilibrium of a firm and industry of a perfectly competitive market can be represented as showing in PICTURE - II.

In the above PICTURE – II each firm is in equilibrium at point A. where Marginal Cost (MC) = Marginal revenue (MR) and MC cuts MR from below as said above. And ‘B’ is the output and ‘P’ is the price.In the case of industry it reached in equilibrium at point ‘E’, where both demand and supply interact with each other or equal.

Related

The Long-Run Period and Secular Period Price Determination Under Perfect Competition

How is Price Determined under Monopoly Market?

What Is a Competitive and Free Marketplace?

Economies of Scale: Meaning and Types

How Do Income Effect, Substitution Effect and Price Effect Influence Consumer's Equilibrium?