DuPont Analysis for a Credit Union

The DuPont Equation or DuPont Identity is not easily applied to the analysis of banks or credit unions. This is because some of the concepts used in the unaltered DuPont Analysis do not lend themselves well to evaluating financial institutions. However, it is not impossible to use this method to analyze performance – several academicians have derived methods for modifying the DuPont System to make it useful in a financial intermediary context.

The benefit of using DuPont Analysis is that it decomposes the credit union’s return on equity into income statement and balance sheet components which provides insights to credit union managers on how to improve financial performance. For the purposes of this discussion, we will explore the modified DuPont System as described in Collier et al (2006) and Saunders (2000) to decompose a hypothetical credit union’s return on equity (ROE) into net profit margin (NPM), Average Total Asset Turnover (ATAT), and the credit union’s Equity Multiplier (EM).

A credit union’s ability to deliver on its ultimate objectives is dependent on strong financial performance. The credit union’s future cash flows and future financial performance are dependent on the investment and financing decisions credit unions make in the present. While a bank will want to choose investment and financing decisions that maximize the value (and thereby, share price) of the bank, a credit union will typically want to maximize the value delivered to members and their communities. Even though a bank and credit union work toward different financial end goals, DuPont Analysis can assist both in providing insight into their ROE performance.

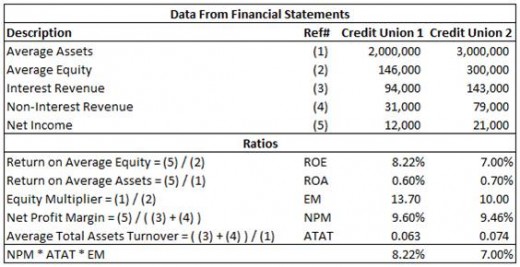

The diagram below provides selected data from the financial statements of two hypothetical credit unions as well as calculations of several ratios that we’ll need to walk through the analysis. ROE can be broken down into Return on Assets (ROA) multiplied by EM. From the diagram below the reader will note that ROA = [Net Income] / [Average Assets] and that EM = [Average Assets] / [Average Equity] so we can see that ROE = ROA * EM. ROA can be further decomposed to [Net Profit Margin] * [Average Total Assets Turnover]. So, ROE is the product of three metrics – NPM * ATAT * EM – where NPM = Net Profit Margin, ATAT = Average Total Assets Turnover, and EM = Equity Multiplier (see the diagram below for more details on these equations).

The larger of our hypothetical credit unions has a lower ROE than the smaller credit union (7.00% versus 8.22%). We can see, though, that the ROA for the larger credit union is better than for the smaller credit union (0.70 versus 0.60). It is the NPM and the EM of the larger credit union that are worse than for the smaller credit union and those two elements are contributing to the smaller ROE metric for the larger credit union.

NPM provides insights into the income statement and its components. ATAT provides insights into the assets section of the balance sheet and EM provides insights into the liabilities and owners equity sections of the balance sheet. It is one thing to know that ROE is improving or worsening over time but it will be a lot more helpful to know why it is improving or worsening. Decomposing ROE into its various income statement and balance sheet metrics provides more information to managers as to why ROE is improving or worsening. For example, knowing why ROE is worsening is necessary so that the right remedies can be applied to the right component(s) that underlie ROE.

References:

Collier, H. W.; McGowan, C. B.; and Muhammad, J.: Financial analysis of financial institutions in an evolving environment 2006. http://ro.uow.edu.au/commpapers/29

Saunders, Anthony. Management of Financial Institutions, Third Edition, McGraw Hill, 2000.

DuPont Analysis Example