FICA Credit Score

What is a Credit Score?

A credit score is a grade that shows your potentiality of getting a loan. Lending institutions rely on your credit score to know whether you’ll be able to pay back a loan on time.

FICA credit score is a 3-digit numerical index which represents an estimate of an individual’s financial credit worthiness. It's a number between 300 to 850 is given to someone to determine one’s credit score.

Just like Paydex Score, your credit score acts as an indicator to potential creditors of how able you are to pay back a loan. The higher your credit score, the higher your chances of getting a loan, as it tells lending institutions you have the potential of offsetting a loan given to you.

There are so many ways to determine the credit score of an individual, top among them the Fair Isaac Corporation (FICA) score. The FICA score, which range from 300-850, is very popular among mortgage lenders who use it to find out which borrowers are probable to default mortgage payments. The other most widely used credit scoring model is the Vantage Score.

If you have a credit score of below 700, you still qualify to get a loan, but with a higher rate of interest. This is because it is the only viable way that your creditor is guaranteed of your ability to pay back.

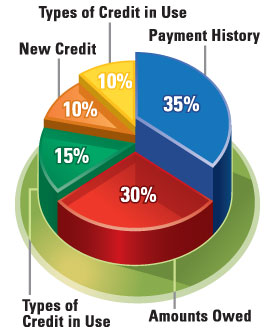

Understanding Your Credit Score

Typically, 35% of your score will be determined by your credit history.

If you have a good credit history, you are guaranteed of a good score,

but if you have a history of bankruptcy or late remittances,

particularly if it is very recent, you will have a low credit score.

30%

of your score will be determined by your outstanding debt; be it a car

loan, home loan, utility debt or credit card debt. It is advisable to

use only 25% or less of your credit limit, to limit the effect it may

have on your credit score.

15% of your score will be determined by the duration that you have had

your credit. The longer the duration the better as it will give your

creditors an opportunity to learn your consumer trends and behavior.

10%

of your debt will be determined by the frequency of your inquiry in the

past. Be advised that if you have so many inquiries, you will create a

bad impression to your creditors that you have a habit of pilling up

debts.

The final 10% will be determined by the type of your existing debt. This encompasses the number of credits and loans accessible to you, and it gets very tricky if you are just starting up on building a credit history.

What is considered a good credit score?

Note

that there is no stipulated pass or fail mark in regard to credit

report, but creditors have set 700 to be a good credit score. 60% of

Americans are capable of achieving this, hence shouldn’t be difficult

for anyone else.

You can improve your credit score

by ensuring you pay your outstanding debts on time. You now can

understand the three figures that appear on your credit card report.

Make a habit to review your credit report and always endeavor to get a credit score of above 700, as that is what is ideal for creditors.

Ways to improve your credit score

- Always pay your bills on time

- Keep your balance low in relation to your available credit - 35% or lower is ideal.

- Make more than the minimum payment

- Pay off credit card debt rather than moving it around to other cards

- Don’t open a lot of new accounts over a short period of time, especially if you have a short credit history

Be advised that your FICA credit score changes each year. And a little self discipline is all it takes to improve your credit score.

- Ways to Settle Tax Debt

There are a number of viable ways to settle tax debt. Which method of settlement you choose should be based on your unique financial situation.

Related

How to Quickly Fix a Bad Credit Score

No Denial Payday Loans: Redefining The Credit Landscape for People With Bad Credit Profiles

Increase Your Credit Score From 550 to 750 in 12 Months

Getting Your First Apartment: A Guide for Young Adults by a Young Adult

Why Your Bank Loan Was Denied or Approved: What Do Loan Officers Look For?