It's Time to Repair Your Credit Score

What is your credit score?

The economy has been rough in the last two decades. Most individuals have lost a job at least once during that time. Job loss is one of the most common reasons individuals are not able to pay bills. Usually unpaid bills commence a domino-effect towards damaged credit reports and scores. Consider beginning the journey to repair your credit score today. If you are indeed seeking a new job, click here to locate a list of the best job search engines and websites.

The key to repairing your credit score is “time”. You will need to pay your bills efficiently over some time (about 4 – 6 months) in order to see your credit score begin to increase effectively (i.e. towards a credit score of 780 perhaps). But have no fear. You can still take action!!! There are actions you can take right now to begin the process of repairing your credit report, ensuring immediate and drastic increases in your credit score. Below you will find a list of procedures to implement for cleaning up your credit report and strengthening your credit score. While several actions are recommended, you should perform actions only as they are applicable to you.

Action 1: Pay off as much of your outstanding balance of debt as possible.

Click here for simple ways to make the money you need to pay off debt without losing a penny. Start your repayment process by consolidating multiple different payments you owe to the same vendor (i.e. college loans, taxes, etc.). Consider paying off the latest overdue and smaller payments first, then move on to the latest overdue and larger payments next. Outstanding vendor payments that are long overdue can enter your credit report at any time. If you are aware of these payments, pay these off first to begin repairing your credit report and score.

Action 2: Get a copy of a current credit report and review the content thoroughly.

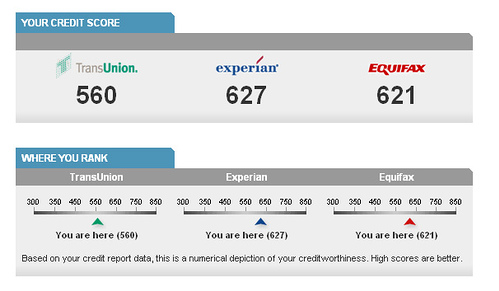

Be certain to use a current credit report to assess the state of your current credit worthiness. There are a number of sites you may visit to obtain a free copy of your credit report, including www.creditkarma.com. You may need to simply sign up on the site to obtain a copy of your report. Refrain from any website that requires the retaining of a credit card on file in order to provide you access to your report. It is recommended, if possible, to obtain a report from all three prominent credit bureaus: TransUnion, Equifax and Experian. Using an older or out-of-date credit report may not reflect any newer entries to your report, as entries are made by creditors or vendors at any given time.

Be certain that you are able to understand your credit report entirely. Some reports are computer-generated for specific use (i.e. banking), so data within that report may not be fully legible or comprehensive to all individuals. Print out a full copy of your report and download an electronic copy to your personal files as well. Take some time to fully review the content of your report. If necessary, feel free to contact the provider of the report with any questions you may have. Again, it is very important that you clearly understand and interpret the content within your credit report.

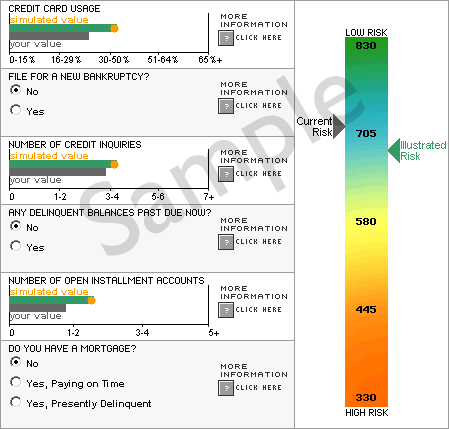

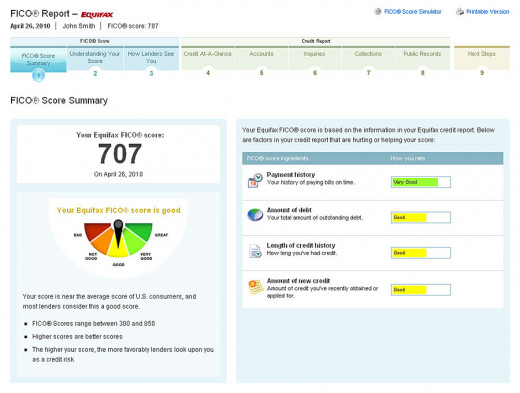

Credit Report Samples

Action 3: Verify the accuracy of credit report information.

After you have reviewed your report completely and can understand the content of your credit report clearly, begin contacting the creditors and vendors that have made entries to your report. Verify the information stated on your report by each creditor or vendor. Request documentation of the content stated. For example, overdue bills must reconcile to at least one paper invoice that was previously sent to you by a vendor or creditor. Reconcile these documents with your files accordingly. The creditor should be able to verify exactly when the bill was sent to your mailing address, as well as if any phone calls were made in an attempt to collect the debt. In the event a creditor cannot verify contacting you in regards to a payment that is claimed due, this entry to your credit report can be refuted with the credit bureaus. (Refuting claims or entries on your credit report will be discussed further below.)

When verifying entries in your credit report, be certain to also follow the paper trail. If a creditor is representing debt transferred from a vendor, consider obtaining the name and contact information of the actual vendor who transferred the debt to that creditor. You should follow-up with the vendor directly to further verify actual amounts due by the claim. Be certain to get the name and contact information of everyone you speak to during this part of the process. Verifying information with a vendor can become tedious and hassling when dishonesty or lack of integrity in managing a customer's financial account information is apparent.

Some vendors may not be accessible by phone, so obtain a mailing address or email address to make contact with the vendor. When emailing or mailing to a physical address for verification of claims, include a copy of only the single page pertaining to the entry in-question made on your credit report. Be sure to first whiteout any personal or additional data from that page on your credit report, such as a social security number, phone numbers, email addresses, mailing address, etc., before mailing the document (unless you plan to be contacted or responded to by the vendor). If the vendor and the claim is legitimate, your account personal information and details should already be in their files. The vendor can use the account number, your name or the amount due to verify the claim within their account records. The vendor should be able to mail or fax to you any documentation available on your past-due account to verify the claim.

If you come across any immediate discrepancies while in conversations with the creditor or vendor, simply request that the errors be fixed or removed from your credit report. Use your own financial files and record-keeping, if applicable, to verify or substantiate any errors in the account information and paperwork of a creditor or vendor. Some vendors will also informally offer you an opportunity to negotiate or pay-off past due payments while in conversation. Be certain to first obtain an email or written agreement confirming that as per discussion or upon payment, the entry on your credit report will be immediately removed. Keep in mind that most vendors will still not remove entries after payment is made, since by law entries can remain on your credit report for up to seven years. While some vendors will remove or adjust entries, many will not remove entries without a formal refute filed or even a court judgment rendered.

Repairing Your Credit

Action 4: File a formal refute against an inaccurate claim made on your credit report.

Incorrect data on your credit report must be updated or removed, as this data will adversely impact your credit score. If a creditor or vendor is refusing to correct inaccurate information on your credit report, then it may be necessary report the inaccurate information directly to the credit bureaus. Write a formal letter to the vendor (or creditor) thoroughly explaining why the information is incorrect, including any solid documentation you may have for your argument. At the end of the letter, inform the vendor that copies of your letter and documentation will be also submitted to the following parties: the three credit bureaus, the local or State General Attorney’s Office, and the Fair Trade Commission (for US residents only) for further investigation. Before mailing the letter to the vendor, make the necessary six copies of all documentation to include in all six of your letters. Mail your letter to the vendor certified mail, if possible, or simply standard mail. In some cases, you may be required to take legal action in a court of law to force vendors or creditors to make changes to your account.

At times you can also make a formal refute of claims on your credit report directly with each credit bureau online. Visit the website of each of credit bureau to find out how to make claims online. Experian, for example, permits individuals to call in refutes and follow-up in a few days. The credit bureau will investigate your refute and work directly with the vendor or creditor to adjust or remove the entry. Keep in mind that entries that are past seven years on your credit report should be refuted for removal as well. Feel free to refute transferred accounts and duplicated information on your credit report, as these are common and quite damaging.

After refuting any credit report entries, be sure to follow-up with changes to your account. Check in to your online credit report profile, if applicable, to verify changes to your report as these may be done automatically. You can also contact the bureaus by phone to follow-up on changes. Regularly and even frequently follow-up with the credit bureaus to confirm that changes to your credit report account are satisfied.

Action 5: Begin the road to increase your score.

Now that your credit report has been updated with accurate information, you now have your correct current credit score. At this time, you will begin the journey to build or increase your credit score. If you have recently repaid or paid off any credit cards, hold off on using these for a while. Maintain a good standing with the credit card vendor for about three months, using cash for transactions. If you do not have any credit cards, it is recommended that you apply for a secure credit card at a bank, such as Citibank, Chase or Capital One. Retain a small overall credit balance (i.e. $200) to begin rebuilding your credit score over time. You will receive the option to increase this amount after a year.

If you have paid off defaulted loans, it is recommended that you refrain from applying for new loans for several months. If your loans are in good standing on the other hand, continue making timely payments on the loans, as this will increase your credit score over time. While opening a mortgage can boost your credit score, a recent foreclosure on a property my not permit you to purchase a new home any time soon. Payments on car leases and mortgages that have been kept up efficiently will also begin to increase your credit score over time. If you find yourself struggling with car lease payments, then consider renting out or selling the car to cover the overall costs. There are a number of ways you can earn income with your car. You can also request decreases in the size of your payments to creditors and vendors to match your current level of income. US Federal student loans providers, for example, can now be paid in accordance with one’s current level of income, as per new mandates under the Obama Administration. The assistance in managing student loan debt has been warmly received by many recent college grads struggling to find stable employment or income today. If you are still borrowing student loans, consider using lower-interest government student loans to pay off higher-interest debts (i.e. credit cards, private loans, etc.). Fortunately, you can consolidate Federal subsidized and unsubsidized school loans into a manageable, single and minimal payment per month.

Action 6: Add accounts that are in good standing to your credit report.

In certain circumstances, you can request from current vendors to add your account with them to your credit report towards increasing your credit worthiness. If the account with the vendor is in excellent standing (i.e. utility accounts, retail accounts, private loans, etc.), then feel free to request that the account is added to your credit report. Once these accounts are added, they will offset adverse information on your credit report and increase your credit score.

Action 7: Refrain from newer hard inquiries and address changes.

Every time your credit report is requested in response to a credit application filed with a vendor, you will receive a hard inquiry on your credit report which reduces your credit score. Similarly, your score is reduced every time you change your home address. Try to refrain from changing residences or submitting credit applications for any reason as best as possible. This may be difficult to accomplish if you are house shopping or car shopping. However, some lenders will review your application and inform you of any possible rejection or approval for loans before formally submitting your loan application. In this way, you will not receive a hard inquiry on your credit report for the transaction.

Action 8: Monitor your report regularly and continuously.

If you do not have a credit report profile, it is recommended that you obtain one as soon as possible. You will need to pay for the opportunity to monitor your credit report online. Sites, such as www.experian.com, will charge a minimal fee to allow you to regularly review and monitor your credit report online. Be diligent in scrutinizing any new data or information added to your credit report account. Immediately correct errors with vendors as they appear on your report, using your own records to substantiate your claims. You may need to formally refute entries to your report as well. While paying your bills efficiently over time will increase your credit score, monitoring your report regularly will ensure the correction of newer negative information on your credit report.

You should finally begin to see increases in your overall credit score. After such an overhaul of your credit report, you should allow at least six months to see a substantial increase in your credit score. If necessary, you may consider explaining to an interested party that you have recently overhauled your credit report, but it has not been fully updated as yet. Feel free to provide the interested party with the documentation of all the repairs you have accomplished on your credit report. Many banks, home owners, employers, etc., will appreciate the work you have done to repair your credit score. Good Luck!

Click here to read more of my financial hubs: http://missinfo.hubpages.com

© 2014 S T Guy

Related

How to Respond to a Debt Collection Letter and What to Include in a Debt Validation Letter

How to Quickly Fix a Bad Credit Score

Why Your Bank Loan Was Denied or Approved: What Do Loan Officers Look For?

No Denial Payday Loans: Redefining The Credit Landscape for People With Bad Credit Profiles

Increase Your Credit Score From 550 to 750 in 12 Months