How to Claim Tax Deductions on Charity Contributions?

The United States' tax system has many different types of deductions. A taxpayer can deduct from taxable income any money spent on state and local taxes, health care, mortgage interest, tax preparation fees and charitable donations. Giving to charity is a great tax planning strategy in arming yourself against money-grabbing government agents because donations to charity are tax deductible expenses.

"You may deduct charitable contributions of money or property made to qualified organizations if you itemize your deductions."

(IRS Publication 78)

So, donations can reduce your taxable income and lower your tax bill. To illustrate, let's suppose you are in the 33% tax bracket and you donate a $100. You save $33 on a donation so the actual cost of your donation is reduced through your savings on your taxes. However, you won't be able to deduct your charitable contributions unless you itemize your tax deductions in order to claim any charity. Your donation to a qualified charity is deductible the same year in which it is made (when the contribution is paid). The value of your charitable deductions can't be more than 50 percent of your adjusted gross income in any single year. Donations exceeding the 50 percent limit can be carried forward to future years.

There are many non-profit organizations providing grants to international causes, registered in the U.S. Out of approximately $300 billion donated to charitable causes by Americans, only about five percent is spent on international causes each year.

Donors can usually choose which grants to support. U.S. based granting organizations include: International Development Exchange, Grassroots International, Oxfam America, Global Fund for Women, Development Gap, Funding Exchange National Grants Program, The Global Exchange. .

Public charities are more common than public charities.

Eligible charity organizations are: churches, synagogues, and other religious organizations, fraternal order/lodge, war veterans' organization, any level of government if the contribution is made for exclusively public purposes, organization dedicated to the improvement of public health in the U.S. or abroad.

Contributions are not tax deductible if given to: political parties/campaigns/action committees, individual people, labor unions, chambers of commerce, or business associations, for-profit schools and hospitals, foreign governments. Not tax deductible contributions are also: the value of a volunteer's time for services rendered to a non-profit organization, fees or dues paid to professional associations and fines or penalties paid to local or state governments.

Cumulative List of Organizations in the IRS Publication 78, lists most qualified organizations.

Type of contribution to a charity

Services

A person volunteering at a non profit (certified charity), is not entitled to a deduction for provided services. The person is entitled to deduct unpaid expenses that incurred in rendering them (out-of-pocket costs such as mileage).

Cash

Generally, there is only one limitation on the total amount that the donor is entitled to deduct: the contribution does not exceed 50% of the adjusted gross income. Amount which isn't deducted in the year of making the contribution may be carried forward (next year for up to 5 years).

Property

The donor is entitled to deduct the value of property (non-cash donations or outdated clothing, household furnishings, or office equipment) on his tax return for that year. According to the IRS, donated goods must be in "good condition or better". Non-cash contributions of property are subject to strict record keeping (any written acknowledgments you receive from the charity and other documentation) and to substantiation rules (assessment of the fair market value of the goods or contributed property).

FMV – Fair Market Value

The Fair market value is defined by the Internal Revenue Service as "the price at which property would change hands between a willing buyer and a willing seller, neither having to buy or sell, and both having reasonable knowledge of all the relevant facts."

The IRS says it's something you have to determine. In order to assign a fair market value to the items that you're donating, you have to follow the rules laid out in Publication 561, Determining the Value of Donated Property and Publication 526, Charitable Contributions.

The deduction for property owned for more than a year, is usually equal to the property's fair market value. The donor is never taxed on the appreciated amount because appreciated property can be deducted at the full fair value of the property. The donee organization doesn't have to pay tax on the appreciation in the property either. You must have a receipt for the goods from the charity to claim a deduction. You can't claim a fair market value that's more than the original cost of that item. A good rule to follow when valuating used items, for example, clothing, is to use 25 percent of the original purchase price as a guide.

Lowering Your Taxes by Claiming Tax Deductions on Charity Contributions

In order to be tax-deductible, your donation (charity contribution) must meet the following criteria:

- donation is actually paid/donated (only then it is deductible).

- donation is contributed to a qualified tax-exempt organization. A tax-exempt, non-profit charitable organization is defined under section 501(c)(3) of the Internal Revenue Service tax code. Donee organizations have to receive their 501(c)(3) tax-exempt status from the IRS but some organizations, like churches and other religious organizations, are not required to obtain the 501(c)(3) status. Political organizations classified as 501 (c) (4) are non-profit, but aren't considered to be charities.

- meeting record keeping

requirements (the donor has saved canceled checks,

acknowledgment letters from the charity and appraisals for donated property). Documentation is the essence of rightful claim for donations – the more

documentation one has, the higher a deduction to claim. Casual donations

dropped into a charity's collection box or bucket cannot be deducted without a

receipt to back up the donor's claim. The Pension Protection Act obliges the donor

to keep written records of all cash donations. The records must indicate the

name of the charitable organization, the date and the amount of contribution. If

the donor receives some goods or services in exchange for his/her donation, the

charity must specify the value of those goods or services. In this case, only the

amount of the donation that is above that value can be deducted.

- A detailed record keeping of donated items includes: (1) the number of items and the condition they're in, (2) the dates when the items are received or bought (if the exact dates are unknown, approximate dates are to be used), (3) the original purchase prices, (4) keeping visual records like for example, a quick snapshot or video of the donated items with your tax records, which substantiates the donor's contribution if questions ever arise, (5) signed and dated donation receipts from the charity organization receiving the donated items.

- donation is contributed by people who are eligible to itemize their deductions. Itemized deductions and the overall total itemized deductions are sometimes limited to a certain threshold amount.

Limits on the Charitable Contribution Deduction

There are limits referring specifically to charitable contributions, and there are general limits on itemized deductions. Limits are relevant only if you contribute more than 20% of your adjusted gross income to charities. You can deduct cash contributions in full up to 50% , property contributions in full up to 30%, and contributions of appreciated capital gains assets in full up to 20% of the adjusted gross income.

Charitable contributions in excess of these limits can be carried over to the following tax year up to a miximum of five years.

Documents and tax forms to report donation

- Written acknowledgment from the charity that received a donation.

- IRS Form 1040 Schedule A – this is where taxpayers tally up their various tax deductions item by item. Charitable deductions are reported on Schedule A (Line 17) of Form 1040. If the amount is over $500 complete and file IRS form 8283.

- Filling the IRS Form 8283, Noncash Charitable Contributions with your return is obligatory if you donate non-cash items with a total value of more than $500. If your claimed deduction is more than $5,000, you must get an appraisal of the property's fair market value.

- An appraisal of the donated item from a qualified appraiser (someone authorized to complete Part III, Declaration of Appraiser, of Section B (form 8283)) goes together with the attachment of an appraisal summary to your tax return.

- IRS Form 1098-C is for contributions of motor vehicles, boats and airplanes. If you contribute a vehicle (car, truck, boat, airplane or other) and the vehicle is worth more than $500, you must also gain a written acknowledgement from the non-profit organization to claim a tax deduction. If the organization has sold the vehicle for an amount lower then the fair market value you can only deduct the sale amount listed on 1098-C.

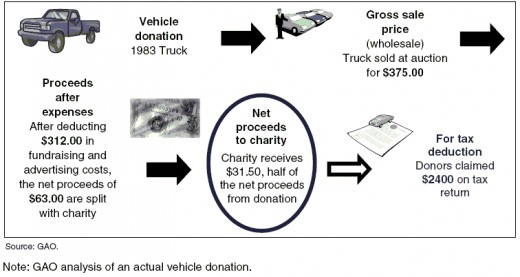

Example to illustrate: Donation of a Vehicle (steps and tax forms)

Claim your tax deduction by placing the fair market value (FMV) amount of the vehicle on Line 17 of the IRS form 1040 Schedule A. In most cases, the value of your car is based on the actual sales price the charity receives when it auctions the car. This rule is for cars worth more than $500. The owner donates the car to the charity, but cannot claim the deduction until the charity sends him a receipt from the sale. FMV of the car may be deducted if the charity keeps the car and uses it, improves it and then sells it, or if the car is sold for less than fair market value to a person with low income.

Confirm the charitable organization is qualified to your donation. If you have doubts or question the organization, take a copy of the IRS publication 78, contact a tax professional or the IRS. In order for you to claim a tax deduction for your donated car, the charity must be classified as a 501 (c) (3) public charity. Just because an organization is classified as non-profit doesn't mean that the IRS will qualify your car donation as a deduction. Pay attention to ads from intermediaries who accept the car and sell it on the charity's behalf, but these for-profit companies may keep up to 90 percent of the money received from the sale of the car. Donate your car directly to the charity meaning you should take it there yourself to save any transport fees the charity may incur maximizing your donation in such way.

Once the organization has sold the vehicle make sure that you assign ownership of your vehicle to the charity, otherwise the car will legally still belong to you and you'll be liable for any tickets or criminal activity related to the car. If your car sells for more than $500, you have to fill in the IRS form 8283 and include it with your annual taxes.

Get an appraisal (for donation exceeding $500) and a written acknowledgement of the donation from the organization in a 1098-C form line 4A to acknowledge the receipt of the vehicle and report the amount if the organization has sold the vehicle.

Input the amount of the donated vehicle on line 17 (IRS Form 1040 Schedule A). This amount is calculated by taking the amount on form 8283 and comparing it to the amount listed on 1098-C line 4A. If the amount on form 1098-C is less then the amount listed on the form 8283 you will use the lesser to the two amounts on line 17 of the 1040 schedule A form. The total of your itemized deductions on 1040 schedule A will be placed on the 1040 form line 40.

Attach your W-2's (Wage and Tax Statement), form 8283 and 1040 schedule A to your 1040 and send to the IRS for processing.

Remember that it's always advisable to consult a tax adviser about specific tax situations.

- What do YOU THINK about organ donation? Share YOUR OPINION!

The main problem in the area of transplantation lies in the fact that the demand for organs still greatly surpasses the number of donors. Public awareness and opinion play an important role in increasing organ donation. You're invited to participate

")