Federal Student Loans: Repaying Student Loan Debt

The most important thing your financial aid adviser will tell you about paying for college is that student loans are DEBT. This means that you are financially obligated to pay these loans back as per the terms of your loan agreement. Defaulting on these loans has the potential to damage your credit, which can exclude you from many aspects of the American lifestyle that require good credit - mortgages for homes, lower rates for cars and trucks, and even small business financing after you graduate college. In most cases, these loans cannot be forgiven or erased through bankruptcy. Repaying your student loans may seem like a daunting task, but there are some very flexible repayment plans that give U.S. students the opportunity to make a dent in their outstanding debt while still maintaining good payment history.

Repayment Plans

With federal education loans, students are able to select a repayment plan that best suits their financial capacity and prior obligations. The repayment plans offered by the Department of Education are flexible and allow students the option to change plans if their employment or income situation changes. Each student may contact their loan service provider to discuss the repayment plan that is best for them or to make any changes to an existing repayment plan. This article gives a brief overview of the available repayment plans for federal student loans. Talk to a financial adviser to determine what is best for your personal finances.

1. Standard

- Fixed monthly payments with a minimum of $50 per month, and a maximum term of 10 years to have the loan(s) paid in full;

- Available for subsidized and unsubsidized Federal Direct Loans, Federal Stafford Loans, and all PLUS loans.

2. Extended

- Fixed or graduated monthly payments with a maximum term of 25 years to have the loan(s) paid in full;

- Available for subsidized and unsubsidized Federal Direct Loans, Federal Stafford Loans, and all PLUS loans.

*Other requirements and restrictions may apply to this repayment plan.

3. Graduated

- Lower monthly payments initially, with an increase in monthly payments every two years and a maximum term of 10 years to have the loan(s) paid in full;

- Available for subsidized and unsubsidized Federal Direct Loans, Federal Stafford Loans, and all PLUS loans.

4. Income-Based

- Maximum monthly payment is 15% of discretionary income - the difference between adjusted gross income and 150% of poverty guidelines - and a maximum term of 25 years to have the loan(s) paid in full;

- Available for subsidized and unsubsidized Federal Direct Loans, Federal Stafford Loans, all PLUS Loans made to students, and Direct or FFEL Consolidation Loans that do NOT include PLUS Loans to parents.

*Other requirements and restrictions may apply to this repayment plan.

5. Income-Contingent

- Monthly payments are calculated annually based on household size, income, and loan amount, and has a maximum term of 25 years to have the loan(s) paid in full;

- Available for subsidized and unsubsidized Federal Direct Loans, Direct PLUS Loans to students, and Direct Consolidation Loans.

*Other requirements and restrictions may apply to this repayment plan.

6. Income-Sensitive

- Monthly payment is based on annual income and changes as income changes, with a maximum term of 10 years to have the loan(s) paid in full;

- Available for subsidized and unsubsidized Federal Stafford Loans, FFEL PLUS Loans, and FFEL Consolidation Loans.

7. Pay As You Earn

- Maximum monthly payment is 10% of discretionary income - the difference between adjusted gross income and 150% of poverty guidelines - and a maximum term of 20 years to have the loan(s) paid in full;

- Available for subsidized and unsubsidized Federal Direct Loans, Direct PLUS loans to students, and Direct or FFEL Consolidation Loans that do NOT include PLUS Loans to parents.

*Other requirements and restrictions may apply to this repayment plan.

Each repayment plan has benefits and disadvantages, so it is important to weigh all of the available options. Repaying student loans is essential to a healthy credit score in the future. These repayment plans may be adjusted to your income, or even forgiven after a maximum number of years. Take the time to contact your loan service provider to see what choices you have and establish a pattern of good payment history now.

Financial Aid Resources

- Repayment Plans | Federal Student Aid

Federal student loan repayment plans include the Standard, Extended, Graduated, Income-Based, Pay As You Earn, Income-Contingent, and Income-Sensitive Plans. - Federal Student Loans: Subsidized and Unsubsidized Direct Loans

Student loans offered by the U.S. government may be subsidized or unsubsidized. This affects when interest begins accumulating, and when repayment is expected. Learn the differences between the types of loans to encourage smarter repayment decisions.

Credit Resources for Students

- Student Loans and Your Personal Credit

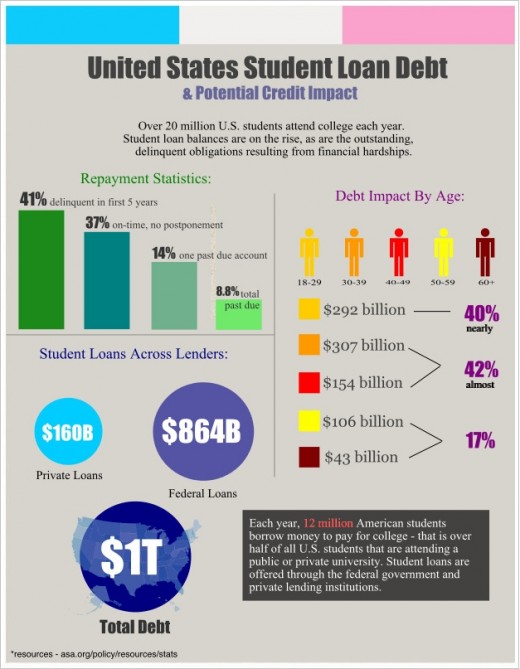

Student loan debt in the United States has reached $1 trillion dollars - over half of all Americans seeking a bachelor's degree have outstanding student loans. Find out how student loans affect your credit report and credit score. - Credit Reports and Credit Scores: How to Improve Credit Applications

Whether putting in credit applications online or in person, these are tips for providing personal information and improving the chances of being approved for credit. - Credit Reports and Credit Scores: Tips for Establishing New Credit

Students just graduating high school or new residents in the U.S. typically start with a blank credit report. Use these tips to establish credit if you have limited or no credit history. - Credit Reports and Credit Scores: Updating Identifying Personal Information

Updating your personal information with the major U.S. credit reports is an important task that may improve your chances of being approved for credit or qualifying for lower interest rates and premiums. - Build Credit with a Laptop Payment Plan

Building credit has become a significant challenge for the average American consumer. There are alternate methods available to help establish credit, such as UpgradeUSA.