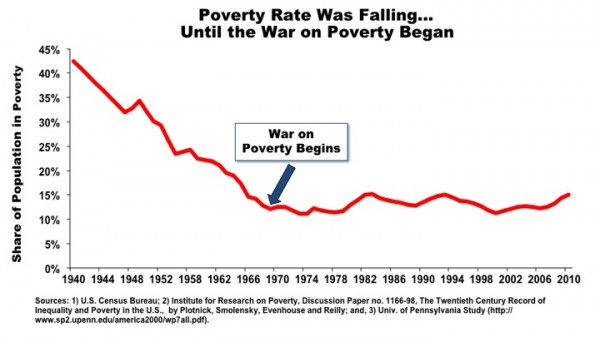

When will they ever learn?

- JaxsonRaineposted 13 years ago

0

0 - JaxsonRaineposted 13 years ago0

Related Discussions

- 620

Is giving money the only way to help poor people?

Is giving money the only way to help poor people?You can't get rid of poverty by giving people money. - P. J. O'Rourke. What do you think?

- 84

Conservatives, Do YOU Feel That Many Poor People Make Excuses ?

Disclaimer: Not addressing the hard working poor who are trying to better lives for their families; the underemployed; the unemployed; the needy elderly; the physically, mentally, emotionally, and psychologically handicapped who CAN'T help themselves; and, those who fell temporarily upon hard...

- 31

what's WRONG with poor people in the united states

[Disclaimer: This post is not referring to the hard-working working poor who want better opportunities for themselves and for their children; the poor who CAN'T help themselves due to being physically, mentally, emotionally, and/or psychologically challenged; our blessed elderly people; the...

- 40

Home Ownership!! What to do, What to do? The American Dream?

American dream of owning a home is dead, majority of renters sayNote: All of the referenced have plenty of graphics for a skim.by The Guardian (Mar 12, 2024)https://www.theguardian.com/society/202 … GTUS_email"The American dream of owning your own home is dead, according to the majority...

- 45

What is the root cause of poverty in the world?

What is the root cause of poverty in the world?

- 78

Are the poor useful for the society in any way?

Are the poor useful for the society in any way?Is it that Poverty and the Poor are mere burden on the society? Do they serve any meaningful purpose?